projectfinance

Step up your finance game.

Option Exercise and Assignment Explained w/ Visuals

Last updated on February 11th, 2022 , 06:38 am

Buyers of options have the right to exercise their option at or before the option’s expiration. When an option is exercised, the option holder will buy (for exercised calls) or sell (for exercised puts) 100 shares of stock per contract at the option’s strike price.

Conversely, when an option is exercised, a trader who is short the option will be assigned 100 long (for short puts) or short (for short calls) shares per contract.

- Long American style options can exercise their contract at any time.

- Long calls transfer to +100 shares of stock

- Long puts transfer to -100 shares of stock

- Short calls are assigned -100 shares of stock.

- Short puts are assigned +100 shares of stock.

- Options are typically only exercised and thus assigned when extrinsic value is very low.

- Approximately only 7% of options are exercised.

The following sequences summarize exercise and assignment for calls and puts (assuming one option contract ):

Call Buyer Exercises Option ➜ Purchases 100 shares at the call’s strike price.

Call Seller Assigned ➜ Sells/shorts 100 shares at the call’s strike price.

Put Buyer Exercises Option ➜ Sells/shorts 100 shares at the put’s strike price.

Put Seller Assigned ➜ Purchases 100 shares at the put’s strike price.

Let’s look at some specific examples to drill down on this concept.

Exercise and Assignment Examples

In the following table, we’ll examine how various options convert to stock positions for the option buyer and seller:

As you can see, exercise and assignment is pretty straightforward: when an option buyer exercises their option, they purchase (calls) or sell (puts) 100 shares of stock at the strike price . A trader who is short the assigned option is obligated to fulfill the opposite position as the option exerciser.

Automatic Exercise at Expiration

Another important thing to know about exercise and assignment is that standard in-the-money equity options are automatically exercised at expiration. So, traders may end up with stock positions by letting their options expire in-the-money.

An in-the-money option is defined as any option with at least $0.01 of intrinsic value at expiration . For example, a standard equity call option with a strike price of 100 would be automatically exercised into 100 shares of stock if the stock price is at $100.01 or higher at expiration.

What if You Don't Have Enough Available Capital?

Even if you don’t have enough capital in your account, you can still be assigned or automatically exercised into a stock position. For example, if you only have $10,000 in your account but you let one 500 call expire in-the-money, you’ll be long 100 shares of a $500 stock, which is a $50,000 position. Clearly, the $10,000 in your account isn’t enough to buy $50,000 worth of stock, even on 4:1 margin.

If you find yourself in a situation like this, your brokerage firm will come knocking almost instantaneously. In fact, your brokerage firm will close the position for you if you don’t close the position quickly enough.

Why Options are Rarely Exercised

At this point, you understand the basics of exercise and assignment. Now, let’s dive a little deeper and discuss what an option buyer forfeits when they exercise their option.

When an option is exercised, the option is converted into long or short shares of stock. However, it’s important to note that the option buyer will lose the extrinsic value of the option when they exercise the option. Because of this, options with lots of extrinsic value remaining are unlikely to be exercised. Conversely, options consisting of all intrinsic value and very little extrinsic value are more likely to be exercised.

The following table demonstrates the losses from exercising an option with various amounts of extrinsic value:

As we can see here, exercising options with lots of extrinsic value is not favorable.

Why? Consider the 95 call trading for $7. Exercising the call would result in an effective purchase price of $102 because shares are bought at $95, but $7 was paid for the right to buy shares at $95.

With an effective purchase price of $102 and the stock trading for $100, exercising the option results in a loss of $2 per share, or $200 on 100 shares.

Even if the 95 call was previously purchased for less than $7, exercising an option with $2 of extrinsic value will always result in a P/L that’s $200 lower (per contract) than the current P/L. F

or example, if the trader initially purchased the 95 call for $2, their P/L with the option at $7 would be $500 per contract. However, if the trader decided to exercise the 95 call with $2 of extrinsic value, their P/L would drop to +$300 because they just gave up $200 by exercising.

7% Of Options Are Exercised

Because of the fact that traders give up money by exercising an option with extrinsic value, most options are not exercised. In fact, according to the Options Clearing Corporation, only 7% of options were exercised in 2017 . Of course, this may not factor in all brokerage firms and customer accounts, but it still demonstrates a low exercise rate from a large sample size of trading accounts.

So, in almost all cases, it’s more beneficial to sell the long option and buy or sell shares instead of exercising. We like to call this approach a “synthetic exercise.”

Congrats! You’ve learned the basics of exercise and assignment. If you’d like to know how the exercise and assignment process actually works, continue to the next section!

Who Gets Assigned When an Option is Exercised?

With thousands of traders long and short options in the market, who actually gets assigned when one of the traders exercises their option?

In this section, we’ll run through the exercise and assignment process for options so you know how the assignment decision occurs.

If a trader is short a single option, how do they get assigned if one of a thousand other traders exercises that option?

The short answer is that the process is random. For example, if there are 5,000 traders who are long a call option and 5,000 traders who are short that call option, an account with the short option will be randomly assigned the exercise notice. The random process ensures that the option assignment system is fair

Visualizing Assignment and Exercise

The following visual describes the general process of exercise and assignment:

If you’d like, you can read the OCC’s detailed assignment procedure here (warning: it’s intense!).

Now you know how the assignment procedure works. In the final section, we’ll discuss how to quickly gauge the likelihood of early assignment on short options.

Assessing Early Option Assignment Risk

The final piece of understanding exercise and assignment is gauging the risk of early assignment on a short option.

As mentioned early, only 7% of options were exercised in 2017 (according to the OCC). So, being assigned on short options is rare, but it does happen. While a specific probability of getting assigned early can’t be determined, there are scenarios in which assignment is more or less likely.

The following scenarios summarize broad generalizations of early assignment probabilities in various scenarios:

In regards to the dividend scenario, early assignment on in-the-money short calls with less extrinsic value than the dividend is more likely because the dividend payment covers the loss from the extrinsic value when exercising the option.

All in all, the risk of being assigned early on a short option is typically very low for the reasons discussed in this guide. However, it’s likely that you will be assigned on a short option at some point while trading options (unless you don’t sell options!), but at least now you’ll be prepared!

Next Lesson

Options Trading for Beginners

Intrinsic and Extrinsic Value in Options Trading Explained

Option Greeks Explained: Delta, Gamma, Theta & Vega

Additional resources.

Exercise and Assignment – CME Group

Learn About Exercise and Assignment – CME Group

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

Navigating exercise & assignment

Exercise & assignment: a cautionary tale

You shake your Magic 8 ball and the screen reads, “Just because you can, doesn’t always mean you should…”

Sage advice, especially when it comes to exercising your options. If you buy calls or puts and decide to do what the option gives you the right to do—buy stock for long call options or sell stock for long put options—it sets off a process called “exercise and assignment.” Normally, this isn’t the road most traders go down. Rather, most traders open options positions with the intent to close them later for a profit—un-exercised. Let’s break things down and take a closer look at the mechanics of exercise and assignment.

The mechanics of exercise & assignment

When you exercise a long call, you convert your call into stock. You’ll actually get 100 shares of the stock for every call you exercise…along with a bill for the cost of the stock, dictated by the strike of the call you’re exercising. For example, if you exercised a call with a strike price of $50, you would buy 100 shares of the underlying stock at $50 per share, for a total cost of $5,000.

Now, your exercise is someone else’s assignment . A randomly selected person who is short that call option receives a notice that they’ve been “assigned” and are required to sell 100 shares of stock for every option they’re assigned.

If we’re talking about put options, when you exercise your put, you’re selling (“putting,” actually) the stock to someone (also nameless) who is short a put on the other side of the trade. They have to buy it.

This great power to exercise is always in the control of the option owner, except at expiration. At that point, options that are in the money, even by just one cent, will be exercised automatically (this is common, but always check with your broker regarding automatic exercise policies).

The good, the bad, the ugly (of exercising)…

First, here are a few scenarios where exercising might be a good idea.

- You were assigned on the short leg of a spread . (More on this below.)

- You really, really want to buy or sell the stock, and you can afford to.

- The option you own is illiquid and the bid/ask spread (the difference between the bid and the ask) is very wide. If you stand to lose more selling the option than simply exercising, it makes sense to go ahead and exercise. You don’t want to sell an option for less than its real value (the value that’s in the money ).

- Sometimes it is worth exercising your long call to collect a dividend. Remember, options owners do not take part in collecting dividends, only stockholders.

Then, here’s why you may not want to exercise.

- Long options are cheaper than long or short stock.

- Long options are lower risk in that only the premium spent is the maximum you can lose when compared to being long or short stock. Even if you can afford the stock position, make sure you want to take on that type of risk.

- You’re simply giving away your money if your option has any time value. Rather than exercise, if you sell your option in order to close, you not only keep that time value, but you can also mitigate the loss due to an early assignment (in the case of a long option that was previously a part of a spread).

- You’re giving away even more money if you exercise an out of the money option. If an option is OTM and you don’t want it anymore, you try to sell it. If there is no value to it, you may want to just let it expire worthless. Who knows, the stock could make a comeback before expiration.

…and now for the Ugly (of Assignment)

Where new options traders can get in a lot of trouble is misunderstanding assignments—particularly when they’re trading spreads, which contain both a long and a short option. Whereas exercising is something you control in a long position, assignment is something that can happen to you at any time while you’re in a short position.

If your short put option goes in the money and you’re assigned, the cash balance in your account might show a large loss equal to the size of the assigned position. If your short call option gets assigned, you might see a short stock position resulting from selling shares you didn’t already own. But fear not! That’s where your long option comes to the rescue.

As soon as you exercise the long option from the spread, you’ll immediately offset the loss, minus the maximum loss of the spread (which is usually the distance between the short and long strikes of the options).

Closing time, time for you to go out…

If you’re speculating with options, exercising is rarely the optimal choice to close your position. However, it’s worth knowing when you should or shouldn’t and what to do when faced with the decision.

If you have a short, deep-in-the-money option and are at risk of being assigned, it’s usually best to close the position and move on prior to expiration. Assignment doesn’t happen all the time, but it’s the reason you never want to “set and forget” about your options trades, particularly spreads with short options. When your short options go in the money, the longer you remain in the position, the greater the chance you have of being assigned.

The Step-by-Step to Exercise

If you need to exercise your long options:

- Open Robinhood, and go to your positions screen by tapping the chart icon in the lower left

- Tap “Exercise,” and follow the instructions

Next up: Risk management

Disclosures

*Content is provided for informational purposes only, does not constitute tax or investment advice, and is not a recommendation for any security or trading strategy. All investments involve risk, including the possible loss of capital. Past performance does not guarantee future results. *

Options trading entails significant risk and is not appropriate for all customers. Customers must read and understand the Characteristics and Risks of Standardized Options before engaging in any options trading strategies. Options transactions are often complex and may involve the potential of losing the entire investment in a relatively short period of time. Certain complex options strategies carry additional risk, including the potential for losses that may exceed the original investment amount.

Robinhood Financial does not guarantee favorable investment outcomes. The past performance of a security or financial product does not guarantee future results or returns. Customers should consider their investment objectives and risks carefully before investing in options. Because of the importance of tax considerations to all options transactions, the customer considering options should consult their tax advisor as to how taxes affect the outcome of each options strategy. Supporting documentation for any claims, if applicable, will be furnished upon request.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock . Securities trading is offered through Robinhood Financial LLC.

The Mechanics of Option Trading, Exercise, and Assignment

Options were originally traded in the over-the-counter ( OTC ) market , where the terms of the contract were negotiated. The advantage of the OTC market over the exchanges is that the option contracts can be tailored: strike prices, expiration dates, and the number of shares can be specified to meet the needs of the option buyer. However, transaction costs are greater and liquidity is less.

Option trading really took off when the first listed option exchange — the Chicago Board Options Exchange ( CBOE )— was organized in 1973 to trade standardized contracts, greatly increasing the market and liquidity of options. The CBOE was the original exchange for options, but, by 2003, it has been superseded in size by the electronic Nasdaq International Securities Exchange (ISE), based in New York. Most options sold in Europe are traded through electronic exchanges. Other exchanges for options in the United States include: New York Stock Exchange , and the NASDAQtrader.com .

Option exchanges are central to the trading of options:

- they establish the terms of the standardized contracts

- they provide the infrastructure — both hardware and software — to facilitate trading, which is increasingly computerized

- they link together investors, brokers, and dealers on a centralized system, so that traders get the best bid/ask prices

- they guarantee trades by taking the opposite side of each transaction

- they establish the trading rules and procedures

Options are traded just like stocks — the buyer buys at the ask price and the seller sells at the bid price . The settlement time for option trades is 1 business day ( T+1 ). However, to trade options, an investor must have a brokerage account and be approved for trading options and must also receive a copy of the booklet Characteristics and Risks of Standardized Options .

The option holder, unlike the holder of the underlying stock, has no voting rights in the corporation, and is not entitled to any dividends. Brokerage commissions are still charged for options even though the commissions for stocks have been free for a while. Prices for most options range from $0.65 to $1 per contract .

The Options Clearing Corporation (OCC)

The Options Clearing Corporation ( OCC ) is the counterparty to all option trades. The OCC issues, guarantees, and clears all option trades involving its member firms, including all U.S. option exchanges, and ensures that sales are transacted according to the current rules. The OCC is jointly owned by its member firms — the exchanges that trade options — and issues all listed options, and controls and effects all exercises and assignments. To provide a liquid market, the OCC guarantees all trades by acting as the other party to all purchases and sales of options.

The OCC, like other clearing companies, is the direct participant in every purchase and sale of an option contract. When an option writer or holder sells his contracts to someone else, the OCC serves as an intermediary in the transaction. The option writer sells his contract to the OCC and the option buyer buys it from the OCC.

The OCC publishes statistics, news on options, and any notifications about changes in the trading rules, or the adjustment of certain option contracts because of a stock split or that were subjected to unusual circumstances, such as a merger of companies whose stock was the underlying security to the option contracts.

The OCC operates under the jurisdiction of both the Securities and Exchange Commission ( SEC ) and the Commodities Futures Trading Commission ( CFTC ). Under its SEC jurisdiction, OCC clears transactions for put and call options on common stocks and other equity issues, stock indexes, foreign currencies, interest rate composites and single-stock futures . As a registered Derivatives Clearing Organization ( DCO ) under CFTC jurisdiction, the OCC clears and settles transactions in futures and options on futures .

The Exercise of Options by Option Holders and the Assignment to Fulfill the Contract to Option Writers

When an option holder wants to exercise his option, he must notify his broker of the exercise, and if it is the last trading day for the option, the broker must be notified before the exercise cut-off time , which will probably be earlier than on trading days before the last day, and the cut-off time may differ for different option classes or for index options. Although policies differ among brokerages, it is the duty of the option holder to notify his broker to exercise the option before the cut-off time.

When the broker is notified, then the exercise instructions are sent to the OCC, which then assigns the exercise to one of its Clearing Members who are short in the same option series as is being exercised. The Clearing Member will then assign the exercise to one of its customers who is short in the option. The customer is selected by a specific procedure, usually on a first-in, first-out basis, or some other fair procedure approved by the exchanges. Thus, there is no direct connection between an option writer and a buyer.

To ensure contract performance, option writers are required to post margin, the amount depending on how much the option is in the money. If the margin is deemed insufficient, then the option writer will be subjected to a margin call. Option holders don't need to post margin because they will only exercise the option if it is in the money. Options, unlike stocks, cannot be bought on margin.

Because the OCC is always a party to an option transaction, an option writer can close out his position by buying the same contract back, even while the contract buyer retains his position, because the OCC draws from a pool of contracts with no connection to the original contract writer and buyer.

A diagram outlining the exercise and assignment of a call.

Example: No Direct Connection between Investors Who Write Options and those Who Buy Them

John Call-Writer writes an option that legally obligates him to provide 100 shares of JXYZ for the price of $30 until April. The OCC buys the contract, adding it to the millions of other option contracts in its pool. Sarah Call-Buyer buys a contract that has the same terms that John Call-Writer wrote — in other words, it belongs to the same option series . However, option contracts have no name on them. Sarah buys from the OCC, just as John sold to the OCC, and she just gets a contract giving her the right to buy 100 shares of JXYZ for $30 per share until April.

Scenario 1 — Exercises of Options are Assigned According to Specific Procedures

In February, the price of JXYZ rises to $35, and Sarah thinks it might go higher in the long run, but since March and April generally are volatile times for most stocks, she decides to exercise her call (sometimes called calling the stock ) to buy JXYZ stock at $30 per share to hold the stock indefinitely. She instructs her broker to exercise her call; her broker forwards the instructions to the OCC, which then assigns the exercise to one of its participating members who provided the call for sale; the participating member, in turn, assigns it to an investor who wrote such a call; in this case, it happened to be John's brother, Sam Call-Writer. John got lucky this time. Sam, unfortunately, either must turn over his appreciated shares of JXYZ, or he'll have to buy them in the open market to provide them. This is the risk that an option writer must take — an option writer never knows when he'll be assigned an exercise when the option is in the money.

Scenario 2 — Closing Out an Option Position by Buying Back the Contract

John Call-Writer decides that JXYZ might climb higher in the coming months, and so decides to close out his short position by buying a call contract with the same terms that he wrote — one that is in the same option series. Sarah, on the other hand, decides to maintain her long position by keeping her call contract until April. This can happen because there are no names on the option contracts. John closes his short position by buying the call back from the OCC at the market price, which may be higher or lower than what he paid, resulting in either a profit or a loss. Sarah can keep her contract because when she sells or exercises her contract, it will be with the OCC, not with John, and Sarah can be sure that the OCC will fulfill the terms of the contract if she exercises it later.

Thus, the OCC allows each investor to act independently of the other .

When the assigned option writer must deliver stock, she can deliver stock already owned, buy it on the market for delivery, or ask her broker to go short on the stock and deliver the borrowed shares. However, finding borrowed shares to short may not always be possible, so this method may not be available.

If the assigned call writer buys the stock in the market for delivery, the writer only needs the cash in his brokerage account to pay for the difference between what the stock cost and the strike price of the call, since the writer will immediately receive cash from the call holder for the strike price. Similarly, if the writer is using margin, then the margin requirements apply only to the difference between the purchase price and the strike price of the option. Full margin requirements, however, apply to shorted stock.

An assigned put writer will need either the cash or the margin to buy the stock at the strike price, even if he intends to sell the stock immediately after the exercise of the put. When the call holder exercises, he can keep the stock or immediately sell it. However, he must have the margin, if he has a margin account, or cash, for a cash account, to pay for the stock, even if he sells it immediately. He can also use the delivered stock to cover a short in the stock. (Note: equity requirements differ because an assigned call writer immediately receives the cash upon delivery of the shares, whereas a put writer or a call holder who purchased the shares may decide to keep the stock.)

Example: Fulfilling a Naked Call Exercise

A call writer receives an exercise notice on 10 call contracts with a strike of $30 per share on JXYZ stock on which she is still short. The stock currently trades at $35 per share. She does not own the stock, so, to fulfill her contract, she must buy 1,000 shares of stock in the market for $35,000 then sell it for $30,000, resulting in an immediate loss of $5,000 minus the commissions of the stock purchase and assignment.

Both the exercise and assignment incur brokerage commissions for both holder and assigned writer. Generally, the commission is smaller to sell the option than it is to exercise it. However, there may be no choice if it is the last day of trading before expiration. Both the buying and selling of options and the exercise or assignment are settled in 1 business day after the trade ( T+1 ).

Often, a writer will want to cover his short by buying the written option back on the open market. However, once he receives an assignment, then it is too late to cover his short position by closing the position with a purchase. Assignment is usually selected from writers still short at the end of the trading day. A possible assignment can be anticipated if the option is in the money at expiration, the option is trading at a discount, or the underlying stock is about to pay a large dividend.

The OCC automatically exercises any option that is in the money by at least $0.01 ( automatic exercise , Exercise-by-Exception , Ex-by-Ex ), unless notified by the broker not to. A customer may not want to exercise an option that is only slightly in the money if the transaction costs would exceed the net profit from the exercise. Despite the automatic exercise by the OCC, the option holder should notify his broker by the exercise cut-off time , which may be before the end of the trading day, of an intent to exercise. Exact procedures depend on the broker.

Any option that is sold on the last trading day before expiration would likely be bought by a market maker. Because a market maker's transaction costs are lower than for retail customers, a market maker may exercise an option even if it is only a few cents in the money. Thus, any option writer who does not want to be assigned should close out his position before expiration day if there is any chance that it will be in the money even by a few pennies.

Early Exercise

Sometimes, an option will be exercised before its expiration day — called early exercise , or premature exercise . Because options have a time value in addition to intrinsic value, most options are not exercised early. However, there is nothing to prevent someone from exercising an option, even if it is not profitable to do so, and sometimes it does occur, which is why anyone who is short an option should expect the possibility of being assigned early.

When an option is trading below parity (below its intrinsic value), then arbitrageurs can take advantage of the discount to profit from the difference, because their transaction costs are very low. An option with a high intrinsic value will have little time value, and so, because of the difference between supply and demand in the market at any given moment, the option could be trading for less than its true worth. An arbitrageur will almost certainly take advantage of the price discrepancy for an instant profit. Anyone who is short an option with a high intrinsic value should expect a good possibility of being assigned an exercise.

Example: Early Exercise by Arbitrageurs Profiting from an Option Discount

JXYZ stock is currently at $40 per share. Calls on the stock with a strike of $30 are selling for $9.80. This is a difference of $0.20 per share, enough of a difference for an arbitrageur, whose transaction costs are typically much lower than for a retail customer, to profit immediately by selling short the stock at $40 per share, then covering his short by exercising the call for a net of $0.20 per share minus the arbitrageur's small transaction costs.

Option discounts will only occur when the time value of the option is small, because either it is deep in the money or the option will soon expire.

Option Discounts Arising from an Imminent Dividend Payment on the Underlying Stock

When a large dividend is paid by the underlying stock, its price drops on the ex-dividend date, resulting in a lower value for the calls. The stock price may remain lower after the payment, because the dividend payment lowers the book value of the company. This causes many call holders to either exercise early to collect the dividend, or to sell the call before the drop in stock price. When many call holders sell at once, the calls sell at a discount to the underlying, creating opportunities for arbitrageurs to profit from the price difference. However, there is risk the transaction will lose money, because the dividend payment and drop in stock price may not equal the premium paid for the call, even if the dividend exceeds the time value of the call.

Example: Arbitrage Profit/Loss Scenario for a Dividend-Paying Stock

JXYZ stock is currently trading at $40 per share and will pay a dividend of $1 the next day. A call with a $30 strike is selling for $10.20, the $0.20 being the time value of the premium. So an arbitrageur decides to buy the call and exercise it to collect the dividend. Since the dividend is $1, but the time value is only $0.20, this could lead to a profit of $0.80 per share, but on the ex-dividend date, the stock drops to $39. Adding the $1 dividend to the share price yields $40, which is still less than buying the stock for $30 + $10.20 for the call. It might be profitable if the stock does not drop as much on the ex-date or it recovers after the ex-date sufficiently to make it profitable. But this is a risk for the arbitrageur, and this transaction is, thus, known as risk arbitrage , because the profit is not guaranteed.

2019 Statistics for the Fate of Options

Data Source: https://www.optionseducation.org/referencelibrary/faq/options-exercise

All option writers who didn't close out their position earlier by buying an offsetting contract made the maximum profit — the premium — on those contracts that expired. Option writers have lost at least something when the option is exercised, because the option holder wouldn't exercise it unless it was in the money. The more the exercised option was in the money, the greater the loss is for the assigned option writer and the greater the profits for the option holder. A closed out transaction could be at a profit or a loss for both holders and writers of options, but closing out a transaction is usually done either to maximize profits or to minimize losses, based on expected changes in the price of the underlying security until expiration.

- Find a Branch

- Schwab Brokerage 800-435-4000

- Schwab Password Reset 800-780-2755

- Schwab Bank 888-403-9000

- Schwab Intelligent Portfolios® 855-694-5208

- Schwab Trading Services 888-245-6864

- Workplace Retirement Plans 800-724-7526

... More ways to contact Schwab

Chat

- Schwab International

- Schwab Advisor Services™

- Schwab Intelligent Portfolios®

- Schwab Alliance

- Schwab Charitable™

- Retirement Plan Center

- Equity Awards Center®

- Learning Quest® 529

- Charles Schwab Investment Management (CSIM)

- Portfolio Management Services

- Open an Account

The Risks of Options Assignment

Any trader holding a short option position should understand the risks of early assignment. An early assignment occurs when a trader is forced to buy or sell stock when the short option is exercised by the long option holder. Understanding how assignment works can help a trader take steps to reduce their potential losses.

Understanding the basics of assignment

An option gives the owner the right but not the obligation to buy or sell stock at a set price. An assignment forces the short options seller to take action. Here are the main actions that can result from an assignment notice:

- Short call assignment: The option seller must sell shares of the underlying stock at the strike price.

- Short put assignment: The option seller must buy shares of the underlying stock at the strike price.

For traders with long options positions, it's possible to choose to exercise the option, buying or selling according to the contract before it expires. With a long call exercise, shares of the underlying stock are bought at the strike price while a long put exercise results in selling shares of the underlying stock at the strike price.

When a trader might get assigned

There are two components to the price of an option: intrinsic 1 and extrinsic 2 value. In the case of exercising an in-the-money 3 (ITM) long call, a trader would buy the stock at the strike price, which is lower than its prevailing price. In the case of a long put that isn't being used as a hedge for a long stock position, the trader shorts the stock for a price higher than its prevailing price. A trader only captures an ITM option's intrinsic value if they sell the stock (after exercising a long call) or buy the stock (after exercising a long put) immediately upon exercise.

Without taking these actions, a trader takes on the risks associated with holding a long or short stock position. The question of whether a short option might be assigned depends on if there's a perceived benefit to a trader exercising a long option that another trader has short. One way to attempt to gauge if an option could be potentially assigned is to consider the associated dividend. An options seller might be more likely to get assigned on a short call for an upcoming ex-dividend if its time value is less than the dividend. It's more likely to get assigned holding a short put if the time value has mostly decayed or if the put is deep ITM and close to expiration with a wide bid/ask spread on the stock.

It's possible to view this information on the Trade page of the thinkorswim ® trading platform. Review past dividends, the price of the short call, and the price of the put at the call's strike price. While past performance cannot be relied upon to continue, this information can help a trader determine whether assignment is more or less likely.

Reducing the risk associated with assignment

If a trader has a covered call that's ITM and it's assigned, the trader will deliver the long stock out of their account to cover the assignment.

A trader with a call vertical spread 4 where both options are ITM and the ex-dividend date is approaching may want to exercise the long option component before the ex-dividend date to have long stock to deliver against the potential assignment of the short call. The trader could also close the ITM call vertical spread before the ex-dividend date. It might be cheaper to pay the fees to close the trade.

Another scenario is a call vertical spread where the ITM option is short and the out-of-the-money (OTM) option is long. In this case, the trader may consider closing the position or rolling it to a further expiration before the ex-dividend date. This move can possibly help the trader avoid having short stock on the ex-dividend date and being liable for the dividend.

Depending on the situation, a trader long an ITM call might decide it's better to close the trade ahead of the ex-dividend date. On the ex-dividend date, the price of the stock drops by the amount of the dividend. The drop in the stock price offsets what a trader would've earned on the dividend and there would still be fees on top of the price of the put.

Assess the risk

When an option is converted to stock through exercise or assignment, the position's risk profile changes. This change could increase the margin requirements, or subject a trader to a margin call, 5 or both. This can happen at or before expiration during early assignment. The exercise of a long option position can be more likely to trigger a margin call since naked short option trades typically carry substantial margin requirements.

Even with early exercise, a trader can still be assigned on a short option any time prior to the option's expiration.

1 The intrinsic value of an options contract is determined based on whether it's in the money if it were to be exercised immediately. It is a measure of the strike price as compared to the underlying security's market price. For a call option, the strike price should be lower than the underlying's market price to have intrinsic value. For a put option the strike price should be higher than underlying's market price to have intrinsic value.

2 The extrinsic value of an options contract is determined by factors other than the price of the underlying security, such as the dividend rate of the underlying, time remaining on the contract, and the volatility of the underlying. Sometimes it's referred to as the time value or premium value.

3 Describes an option with intrinsic value (not just time value). A call option is in the money (ITM) if the underlying asset's price is above the strike price. A put option is ITM if the underlying asset's price is below the strike price. For calls, it's any strike lower than the price of the underlying asset. For puts, it's any strike that's higher.

4 The simultaneous purchase of one call option and sale of another call option at a different strike price, in the same underlying, in the same expiration month.

5 A margin call is issued when the account value drops below the maintenance requirements on a security or securities due to a drop in the market value of a security or when buying power is exceeded. Margin calls may be met by depositing funds, selling stock, or depositing securities. A broker may forcibly liquidate all or part of the account without prior notice, regardless of intent to satisfy a margin call, in the interests of both parties.

Just getting started with options?

More from charles schwab.

Today's Options Market Update

Weekly Trader's Outlook

Managing Short Call Verticals | Tradecraft

Related topics.

Options carry a high level of risk and are not suitable for all investors. Certain requirements must be met to trade options through Schwab. Please read the options disclosure document titled Characteristics and Risks of Standardized Options before considering any options transaction. Supporting documentation for any claims or statistical information is available upon request.

With long options, investors may lose 100% of funds invested.

Spread trading must be done in a margin account.

Multiple leg options strategies will involve multiple commissions.

Commissions, taxes and transaction costs are not included in this discussion, but can affect final outcome and should be considered. Please contact a tax advisor for the tax implications involved in these strategies.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Exercising Options

The holder of an american-style option can exercise his right to buy (in the case of a call) or to sell (in the case of a put) the underlying shares of stock. .

They first must direct their brokerage firm to submit an exercise notice to OCC. For an option holder to ensure that they exercise the option on that particular day, the holder must notify his brokerage firm before that day’s cut-off time for accepting exercise instructions.

The brokerage firm notifies OCC that an option holder wishes to exercise an option. OCC then randomly assigns the exercise notice to a clearing member. For an investor, this is generally his brokerage firm chosen at random from a total pool of such firms. The firm must then assign one of its customers who has written (and not covered) that particular option.

Assignment to a customer is either random or on a first-in-first-out basis. This depends on the firm’s method. Ask your brokerage firm which method it uses for assignments.

The holder of an American-style option contract can exercise the option at any time before expiration. Therefore, an option writer may be assigned an exercise notice on a short option position at any time before expiration. If an option writer is short an option that expires in-the-money, they should expect assignment on that contract, though assignment is not guaranteed as some long in-the-money option holders may elect not to exercise in-the-money options. In fact, some option writers are assigned on short contracts when they expire exactly at-the-money or even out-of-the money. This occurrence is usually not predictable.

To avoid assignment on a written option contract on a given day, the position must be closed out before that day's market close. Once assignment is received, an investor has no alternative but to fulfill assignment obligations per the terms of the contract.

There is generally no exercise or assignment activity on options that expire out-of-the-money. Owners usually let them expire with no value. Although this is not always the case as post-market underlying moves may lead to out-of-the-money options being exercised and in-the-money options not being exercised.

READ MORE ON ASSIGNMENT (PDF)

What's the Net?

When an investor exercises a call option, the net price paid for the underlying stock on a per share basis is the sum of the call's strike price plus the premium paid for the call. Likewise, when an investor who has written a call contract is assigned an exercise notice on that call, the net price received on per share basis is the sum of the call's strike price plus the premium received from the call's initial sale.

When an investor exercises a put option, the net price received for the underlying stock on per share basis is the sum of the put's strike price less the premium paid for the put. Likewise, when an investor who has written a put contract is assigned an exercise notice on that put, the net price paid for the underlying stock on per share basis is the sum of the put's strike price less the premium received from the put's initial sale.

Early Exercise/Assignment

For call contracts, owners might exercise early to own the underlying stock to receive a dividend. Check with your brokerage firm on the advisability of early call exercise.

It is extremely important to realize that assignment of exercise notices can occur early, days or weeks in advance of expiration day. Investors should expect this as expiration nears with a call considerably in-the-money and a sizeable dividend payment approaching. Call writers should be aware of dividend dates and the possibility of early assignment.

When puts become deep in-the-money, most professional option traders exercise before expiration. Therefore, investors with short positions in deep in-the-money puts should be prepared for the possibility of early assignment on these contracts.

Volatility is the tendency of the underlying security's market price to fluctuate up or down. It reflects a price change's magnitude. It does not imply a bias toward price movement in one direction or the other. It is a major factor in determining an option's premium.

The higher the volatility of the underlying stock, the higher the premium. This is because there is a greater possibility that the option will move in-the-money. Generally, as the volatility of an underlying stock increases, the premiums of both calls and puts overlying that stock increase and vice versa.

Get the Reddit app

Let's Talk About: Exchange Traded Financial Options -- Options Fundamentals -- The Greeks -- Strategies -- Current Plays and Ideas -- Q&A -- **New Traders**: See the Options Questions Safe Haven weekly thread

Exercise & Assignement - A Guide

Exercise & Assignment: There are many questions asked over and over with exercise and assignment being among the most common and repetitive. I was asked to put together a guide that can hopefully be used to answer many of these so here it is!

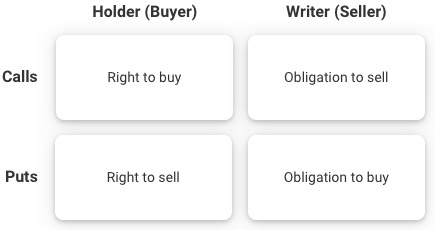

Buyer and Seller Definitions:

- Option Buyer: Purchases the option from the option writer/seller and pays them a premium. The buyer has the right to exercise the option at any time and assign stock to the seller that they are obligated to buy or sell (based on the type of option) at the strike price. The buyer profits from the option price going up.

- Option Writer/Seller: Writes and sells the option to the buyer and collects the premium. The seller has the obligation to take an assignment of the stock at the strike price if the buyer exercises the option. The seller profits if the option price goes down.

Buyer FAQs: (Seller FAQ below)

Q1: As the option buyer do I have to exercise to collect the profit?

A1: No! Any option can be closed to immediately collect any profit and save the cost, plus the risk and time of the exercise process. Exercising early will forgo any extrinsic value that could be captured by just closing the option and is another disadvantage of exercising.

Q2: If I Sell to Close am I under any obligation to be assigned stock should the option be exercised in the future?

A2: No! Once an option is closed there is no longer any rights or obligations regardless of what any future trader does with that option.

Q3: As the buyer, I thought I had no risk of being assigned stock, but after my long option expired I got assigned. How did this happen?

A3: Your option was ITM when it expired, and standard broker policy is to exercise any long option that is .01 or more ITM. This means your option was profitable and the broker exercised it to protect that profit which resulted in stock being assigned. To prevent this from happening simply close the option and collect the profit prior to it expiring. The position should still be at a profit so the stock can be sold (or bought) to collect it.

Q4: When would I want to exercise an option vs. just closing it?

A4: There are very few occasions when exercising makes more sense than closing, but one is if you want to own the stock at the strike price. Because exercising is costly, adds risk and time it is usually better to close the option to collect the profit and then use that profit to help buy the stock outright. On a rare occasion, you can exercise a long leg to cover a short leg assignment.

Q5: Should I be concerned with the short leg of my Debit spread being assigned?

A5: No, if the short leg gets assigned this means the long leg is well ITM and profitable. Just close the long leg to collect the profit and then close the stock position, or exercise the long leg to cover the assignment but remember the costs, risks and time of exercising can cause unnecessary losses.

Seller FAQs:

Q6: Can my short option be assigned early? If so, how often does this happen?

A6: Yes! The option buyer can exercise at any time, but the odds of this are very low. Data varies over time, but over 70% of options are closed with 25% expiring worthless and only about 5% of all options being exercised. Of that 5% there are many traders whose strategy is to be assigned and then a lot more where the option is exercised at expiration, so the amount of options assigned early is a very small percentage.

Q7: How do I know if I am in danger of being assigned early?

A7: There is no way to tell with certainty if you will be assigned, but the farther ITM and the closer the option gets to expiration the odds go up. If you have an option that is well ITM and expiring in a week or less, then closing or rolling it would be advised if you do not wish to be assigned.

Q8: What is short call dividend risk?

A8: Short call options have a dividend assignment risk on the day prior to the stocks ex-dividend date and this video will help understand the risk - https://optionalpha.com/members/knowledge-base#13 If your call option is at risk either close or roll it to avoid being assigned and be aware you could be responsible to pay the option buyer the dividend even if you don't collect it.

Q9: What happens if I am assigned and don't have the money to pay for the stock?

A9: Most full-service brokers will issue a "margin call" to you indicating you have exceeded your account balance and then give you 2 or 3 days to bring your account balance back to even or above. Usually just closing out the stock position will bring the account back to a positive balance, but adding cash will do so as well. If you do not close the stock position or add cash then the broker will liquidate this or other positions as needed. Being assigned without having the cash is really not a big deal and communicating with your broker on your plan will go a long way with them to work with you for the best possible result. However, if you do this routinely the broker may reduce your options trading level or close your account.

Q10: I was assigned stock, what can I do?

A10: You can just buy or sell to close the stock position and take about the same loss as the option position was in. If you can afford to hold the long stock or short stock then selling covered calls or covered puts accordingly can help bring in more premium to possibly break even or profit over time.

Q11: Can the short leg of a credit spread be assigned? If so, won't the broker just exercise the long leg to cover it?

A11: Yes, any short option can be assigned at any time the buyer exercises it. If this happens you can close the long leg that has usually gone up in value to help the P&L, and the result is usually around the same max loss of the spread when opened. If the short leg is ITM, or very close, but the long leg is not, then there is a chance the short leg will be assigned and the long leg will expire worthless perhaps causing a larger loss. Closing the short leg or position will take off any risk, or it can be rolled to reduce the risk. No, the broker will not usually exercise your long option early, and will only exercise it if it is .01 or more ITM at expiration as noted in Q3 above. It is up to you to manage your trades and you should not expect the broker to do that for you, even if it seems obvious.

Resources on Exercise & Assignment:

- OIC Options Assignment FAQs - https://www.optionseducation.org/referencelibrary/faq/options-assignment

- CBOE Quick Facts - http://www.cboe.com/education/getting-started/quick-facts/expiration-exercise-assignment

- OA Options Assignment process - https://optionalpha.com/members/video-tutorials/options-expiration/options-assignment-process

- TT Assignment - https://www.tastytrade.com/tt/learn/assignment

Edited for formatting and additional detail.

Please feel free to add to this list with any questions not covered above! -Scot out!

By continuing, you agree to our User Agreement and acknowledge that you understand the Privacy Policy .

Enter the 6-digit code from your authenticator app

You’ve set up two-factor authentication for this account.

Enter a 6-digit backup code

Create your username and password.

Reddit is anonymous, so your username is what you’ll go by here. Choose wisely—because once you get a name, you can’t change it.

Reset your password

Enter your email address or username and we’ll send you a link to reset your password

Check your inbox

An email with a link to reset your password was sent to the email address associated with your account

Choose a Reddit account to continue

- Why Merrill

- Open An Account

- Why Choose Merrill

- Pricing & Fees

- BofA Preferred Rewards

- Investing & Banking Connected

- Mobile Investing

- Sustainable Investing

- Awards & Accolades

888.637.3343

To find the small business retirement plan that works for you, contact:

Learn more about an advisor's background on FINRA's BrokerCheck

- Personalized Investment Options

- Merrill Edge ® Self-Directed

- Merrill Guided Investing

- Invest with an Advisor

- Compare All

- General Investing

- Education Accounts

- Mutual Funds

- Fixed Income & Bonds

- Margin Trading

- Order Execution Quality

- Idea Builder

- Merrill Edge MarketPro ®

- Early in Your Career

- Peak Earning Years

- Nearing Retirement

- In Retirement

- View all Tools

- Tax Resources

- Plan for College

- College Cost Calculator

- 529 Plan State Tax Calculator

- Plan for Retirement

- Personal Retirement Calculator

- Retirement Account Selector Tool

- 401(k) Rollover Calculator

- Traditional IRA

- Income in Retirement

- Retirement Account Types

- Retirement Tools

- Small Business 401(k)

- Individual 401(k)

- View All Plans

- Get Started Investing

- Investing Basics

- Advanced Investing

- Market & Investing Insights

- Account Options

- Individual Investing Account

- Joint Investing Account

- Custodial Investing Account

- Traditional Inherited IRA

- Roth Inherited IRA

- 529 College Savings Plans

- Custodial UGMA/UTMA Accounts

- Business Investor Account

- lnvesting Costs & Fees

- Pricing & Fees

- Investing & Banking Connected

- Awards & Accolades

- Merrill Edge ® Self-Directed

- Investing with an Advisor

- Compare all

- Fixed Income & Bonds

- Merrill Edge MarketPro ®

- Retirement Account Selector

- 401(k) Rollover Tool

- View all tools

- New to Investing

- Tax Plannning

- Investing by Life Stages

- View all plans

- Market & Investing Insights

- Help When You Want It Find answers to common questions at Merrill Schedule an appointment with Merrill To find the small business retirement plan that works for you, contact: [email protected]

Exercising Options

Submitting exercise or do-not-exercise instructions:.

- All Instructions must be called in and are only applicable to long positions

- Do-Not-Exercise instructions can only be submitted the day of expiration up through market close

- Exercise instructions can be submitted at any time until expiration

- Merrill may take action at any time to close out positions that may not be able to be supported if exercised/assigned. It is extremely important to monitor your open options positions and be aware of your risk exposure.

What's the Net?

Automatic exercise/ assignment, early exercise/assignment, without the jargon, what are options, what are the types of options, what are the greeks, similar articles, options pricing, equity option basics, equity index options.

This material is not intended as a recommendation, offer or solicitation for the purchase or sale of any security or investment strategy. Merrill offers a broad range of brokerage, investment advisory (including financial planning) and other services. Additional information is available in our Client Relationship Summary (PDF) .

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

| Are Not Deposits | Are Not Insured by Any Federal Government Agency | Are Not a Condition to Any Banking Service or Activity |

I'd Like to

- Create an Emergency Fund

- Create an Investment Strategy

- Open an Account with Merrill

Discover Merrill

- Bank of America Preferred Rewards

- Online Trading

- Awards & Recognition

Representatives are available 24/7

Unlimited $0 Trades

Investing in securities involves risks, and there is always the potential of losing money when you invest in securities.

The performance data contained herein represents past performance which does not guarantee future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance information current to the most recent month end, please contact us.

Net Asset Value (NAV) returns are based on the prior-day closing NAV value at 4 p.m. ET. NAV returns assume the reinvestment of all dividend and capital gain distributions at NAV when paid.

Market price returns are based on the prior-day closing market price, which is the average of the midpoint bid-ask prices at 4 p.m. ET. Market price returns do not represent the returns an investor would receive if shares were traded at other times.

Returns include fees and applicable loads. Since Inception returns are provided for funds with less than 10 years of history and are as of the fund's inception date. 10 year returns are provided for funds with greater than 10 years of history.

Before investing consider carefully the investment objectives, risks, and charges and expenses of the fund, including management fees, other expenses and special risks. This and other information may be found in each fund's prospectus or summary prospectus, if available. Always read the prospectus or summary prospectus carefully before you invest or send money. Prospectuses can be obtained by contacting us.

Expense Ratio – Gross Expense Ratio is the total annual operating expense (before waivers or reimbursements) from the fund's most recent prospectus. You should also review the fund's detailed annual fund operating expenses which are provided in the fund's prospectus.

This material is not intended as a recommendation, offer or solicitation for the purchase or sale of any security or investment strategy. Merrill offers a broad range of brokerage, investment advisory (including financial planning) and other services. Additional information is available in our Client Relationship Summary (Form CRS) (PDF) .

Banking products are provided by Bank of America, N.A. and affiliated banks, Members FDIC and wholly owned subsidiaries of Bank of America Corporation ("BofA Corp.").

Merrill Lynch Life Agency Inc. (MLLA) is a licensed insurance agency and wholly owned subsidiary of BofA Corp.

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

| Are Not Deposits | Are Not Insured by Any Federal Government Agency | Are Not a Condition to Any Banking Service or Activity |

© 2024 Bank of America Corporation. All rights reserved.

What is an Assignment in Options?

How does assignment work, what does “write an option” mean, how do you know if an option position will be assigned, what happens after an option is assigned, short put vs. short call, option assignment examples, option assignment summed up, supplemental content, what is an option assignment & how does it work.

Options assignment refers to the process in which the obligations of an options contract are fulfilled. This happens when the holder of an options contract decides to exercise their rights.

When an option holder decides to exercise, the Options Clearing Corporation (OCC) will randomly assign the exercise notice to one of the option writers.

A call option gives the holder the right to buy an underlying asset at a specified price (the strike price) within a certain period. If the holder decides to exercise a call option, the seller (writer) of the option is obligated to sell the underlying asset at the strike price. In this case, the option seller is said to be "assigned."

A put option gives the holder the right to sell an underlying asset at a specified price within a certain period. If the holder decides to exercise a put option, the seller of the option is obligated to buy the underlying asset at the strike price. Again, the option seller is "assigned" in this scenario.

Importantly, being assigned on an option can lead to significant financial obligations, particularly if the option writer does not already own the underlying asset for a call option (known as a naked call) or does not have the cash to buy the underlying asset for a put option. Therefore, option writers should be prepared for the possibility of assignment.

Options assignment works in tandem with the exercise of an options contract. It's the process of fulfilling the obligations of the options contract when the option holder decides to exercise their contractual right as outlined above.

When an option owner exercises their right to convert the option to stock, the option writer is assigned and the option is converted to 100 shares of stock per option contract. Simply put, assignment refers to an options contract being converted to 100 shares of stock, regardless of whether it is a naked option or part of a multi-leg options strategy.

Long call options convert to 100 shares of long stock, and short call options convert to 100 shares of short stock at the strike price.

Long put option contracts convert to 100 shares of short stock, and short put option contracts convert to 100 shares of long stock at the strike price.

In general, the options assignment process includes four steps, as outlined below:

Option Exercise : The holder of the option (the investor who purchased the option) decides to exercise the option. This decision is typically made when it is beneficial for the option holder to do so. For example, if the market price of the underlying asset is favorable compared to the strike price in the option contract.

Notification : When the option is exercised, the Options Clearing Corporation (OCC) is notified. The OCC then selects a member brokerage firm, which in turn chooses one of its clients who has written (sold) an options contract of the same series (same underlying asset, strike price, and expiration date) to be assigned.

Assignment : The selected option writer (the investor who sold the option) is then assigned by the brokerage. The assignment means that the option writer now has the obligation to fulfill the terms of the options contract.

Fulfillment : If it was a call option that was exercised, the assigned writer must sell the underlying asset to the option holder at the agreed-upon strike price. If it was a put option that was exercised, the assigned writer must buy the underlying asset from the option holder at the strike price.

It's important to note that assignment cannot happen when the market is open - these transactions take place when the options market is closed.

Writing an option refers to the act of selling an options contract.

This term is used because the seller is essentially creating (or "writing") a new contract that gives the buyer the right, but not the obligation, to buy or sell a security at a predetermined price within a specific period. In this case, "writing a put or call" and "shorting a put or call" refers to the same thing.

There are two types of options that investors/traders can write: a call option or a put option. Further details for each are outlined below:

Writing a Call Option : This process involves selling someone the right to buy a security from you at a specified price (the strike price) before the option expires. If the buyer decides to exercise their right, you, as the writer, must sell them the security at that strike price, regardless of the market price. If you don't own the underlying security, this is known as writing a naked call, which can involve substantial risk as there is no cap to how high a stock price can go. A short call holder assumes the risk of 100 shares of short stock above the strike price.

Writing a Put Option : This process involves selling someone the right to sell a security to you at a specified price before the option expires. If the buyer decides to exercise their right, you, as the writer, must buy the security from them at that strike price, regardless of the market price. A short put holder assumes the risk of 100 shares of long stock below the strike price.

When an investor/trader writes an option, he/she receives the option’s extrinsic value premium associated with assuming the intrinsic value risk of the options contract. This extrinsic value premium is theirs to keep if held through expiration, regardless of whether the option is exercised or expires worthless.

As such, writing options (i.e. selling options) is typically reserved for experienced investors/traders who are comfortable with the risks involved, as short options assume the risk of 100 shares of long or short stock depending on the options type.

It’s impossible to know for certain if a given option will be assigned, but the more extrinsic value there is associated with an option, the less likely it is to be assigned (excluding dividend risk associated with ITM short call options).

There are several situations in which an options assignment becomes more likely, as detailed below:

In-the-money (ITM) Options : An option is more likely to be exercised, and therefore assigned, if it's in the money . That means the market price of the underlying asset is above the strike price for a call option, or below the strike price for a put option. This is because exercising the option in such a scenario could start to make sense for the option owner as the option would have intrinsic value. OTM options are not likely to be assigned as the trader or investor could just buy or sell shares of stock at a better price in the outright market.

Near Expiration : Options are also more likely to be exercised as they approach their expiration date, particularly if they are in the money. This is because the extrinsic value of the option (a component of its price) diminishes as the option nears expiration, leaving only the intrinsic value (the difference between the market price of the underlying asset and the strike price).

Dividend Payments : For ITM call options, if the underlying security is due to pay a dividend, and the amount of the dividend is larger than the extrinsic value remaining in the option's price, it might make sense for the holder to exercise the option early to capture the dividend. This could lead to early assignment for the writer of the option.

Remember, even if the above scenarios exist, it does not guarantee assignment, as the option holder might not choose to exercise the option. The decision to exercise is entirely up to the option holder.

Therefore, when writing (i.e. selling) options, investors and traders should be prepared for the possibility of assignment at any time until the option expires.

Remember, as the writer of the option, you receive and keep the premium regardless of whether the option is exercised or not. But this premium may not be sufficient to offset any loss from the assignment. That's why writing options involves risk and requires careful consideration.

This term is used because the seller is essentially creating (or "writing") a new contract that gives the buyer the right, but not the obligation, to buy or sell a security at a predetermined price within a specific period.

Writing a Call Option : This process involves selling someone the right to buy a security from you at a specified price (the strike price) before the option expires. If the buyer decides to exercise their right, you, as the writer, must sell them the security at that strike price, regardless of the market price. If you don't own the underlying security, this is known as writing a naked call, which can involve substantial risk.

Writing a Put Option : This process involves selling someone the right to sell a security to you at a specified price before the option expires. If the buyer decides to exercise their right, you, as the writer, must buy the security from them at that strike price, regardless of the market price.

1. Call Option Assignment:

Imagine a scenario in which you've written (sold) a call option for ABC stock. The call option has a strike price of $60 and the expiration date is in one month. For selling this option, you've received a premium of $5.

Now, let's say the stock price of ABC stock shoots up to $70 before the expiration date. The option holder can choose to exercise the option since it is now "in-the-money" (the current stock price is higher than the strike price). If the option holder decides to exercise their right, you, as the writer, are then assigned.

Being assigned means you have to sell ABC shares to the option holder for the strike price of $60, even though the current market price is $70. If you already own the ABC shares, then you simply deliver them. If you don't own them, you must buy the shares at the current market price ($70) and sell them at the strike price ($60), incurring a loss.

2. Put Option Assignment:

Suppose you've written a put option for XYZ stock. The put option has a strike price of $50 and expires in one month. You receive a premium of $5 for writing this option.

Now, if the stock price of XYZ stock drops to $40 before the option's expiration date, the option holder may choose to exercise the option since it's "in-the-money" (the current stock price is lower than the strike price). If the holder exercises the option, you, as the writer, are assigned.

Being assigned in this scenario means you have to buy XYZ shares from the option holder at the strike price of $50, even though the current market price is $40. This means you pay more for the stock than its current market value, incurring a loss.

As such, writing options (i.e. selling options) is typically reserved for experienced investors/traders who are comfortable with the risks involved.

What does an option assignment mean?

What happens when a call is assigned.

If it was a call option that was exercised, the assigned writer must sell the underlying asset to the option holder at the agreed-upon strike price.

What happens when a short option is assigned?

How often do options get assigned.

The frequency with which options get assigned can vary significantly, depending on a number of factors. These can include the type of option, its moneyness (whether it's in, at, or out of the money), time to expiration, volatility of the underlying asset, and dividends.

According to FINRA , only about 7% of options positions are typically exercised. But that does not imply that investors can expect to be assigned on only 7% of their short positions. Investors may have some, all, or none of their short options positions assigned.

How often do options get assigned early?

According to FINRA , only 7% of all options are exercised, which indicates that early assignment options constitute an even lower percentage of the total than 7%.

How late can options be assigned?

In most cases, options can be exercised (and thus assigned to the writer) at any time up to the expiration date for American style options. However, the exact timing can depend on the rules of the specific exchange where the option is traded.

Typically, the holder of an American style option has until the close of business on the expiration date to decide whether to exercise it. Once the decision is made and the exercise notice is submitted, the Options Clearing Corporation (OCC) randomly assigns the exercise notice to one of the member brokerage firms with clients who have written (sold) options in the same series. The brokerage firm then assigns one of its clients.

Do I keep the premium if I get assigned?

As the writer of the option, you receive and keep the premium regardless of whether the option is exercised or not. But this premium may not be sufficient to offset any loss from the assignment. That's why writing options involves risk and requires careful consideration.

Episodes on Assignment

No episodes available at this time. Check back later!

tasty live content is created, produced, and provided solely by tastylive, Inc. (“tasty live ”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tasty live , through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tasty live is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tasty live is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures .

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tasty live (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tasty live is the parent company of tastytrade.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tasty live nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2024 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tasty live ’s podcasts as necessary to view for personal use. tasty live was previously known as tastytrade, Inc. tasty live is a trademark/servicemark owned by tastylive, Inc.

Options Exercise, Assignment, and More: A Beginner's Guide

So your trading account has gotten options approval, and you recently made that first trade—say, a long call in XYZ with a strike price of $105. Then expiration day approaches and, at the time, XYZ is trading at $105.30.

Wait. The stock's above the strike. Is that in the money 1 (ITM) or out of the money 2 (OTM)? Do I need to do something? Do I have enough money in my account? Help!

Don't be that trader. The time to learn the mechanics of options expiration is before you make your first trade.

Here's a guide to help you navigate options exercise 3 and assignment 4 —along with a few other basics.

In the money or out of the money?

The buyer ("owner") of an option has the right, but not the obligation, to exercise the option on or before expiration. A call option 5 gives the owner the right to buy the underlying security; a put option 6 gives the owner the right to sell the underlying security.