The Libor Case: A Focus on Barclays

- First Online: 16 April 2016

Cite this chapter

- Rosella Carè 3

1139 Accesses

The purpose of this chapter is to describe the reputational impact of the Libor case on Barclays by outlining the ensuing process of rebuilding trust and implementing cultural changes. This chapter is organized as follows. First, we briefly describe the major elements of the Libor scandal, including the investigations, fines and regulatory actions. Then, we propose a focus on Barclays, the company that arguably experienced the most significant impact of the media scandal in 2012. In our case study, we describe the course of events that led Barclays into a reputational crisis, identify and describe the core elements of the restructuring concept. In closing, we consider the lessons learned from this series of events.

This is a preview of subscription content, log in via an institution to check access.

Access this chapter

Subscribe and save.

- Get 10 units per month

- Download Article/Chapter or eBook

- 1 Unit = 1 Article or 1 Chapter

- Cancel anytime

- Available as PDF

- Read on any device

- Instant download

- Own it forever

- Available as EPUB and PDF

- Compact, lightweight edition

- Dispatched in 3 to 5 business days

- Free shipping worldwide - see info

- Durable hardcover edition

Tax calculation will be finalised at checkout

Purchases are for personal use only

Institutional subscriptions

Similar content being viewed by others

‘Rough Winds Do Shake the Darling Buds of May’: Theresa May, British Public Diplomacy and Reputational Security in the Era of Brexit

Crafting anti-corruption agencies’ bureaucratic reputation: an uphill battle

Big Law in Venezuela: From Globalization to Revolution

In April 2013, the FSA was replaced by two new regulatory bodies, the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA).

The term ‘Barclays’ refers both to “Barclays Plc Group” and to “Barclays Bank Plc”. For this chapter, we used documents published on the Barclays web site ( http://www.barclays.com/ ) related to both Barclays Plc Group and to Barclays Bank Plc to obtain a complete picture of the company’s historical evolution.

Automated keyword-based searches of online news archives in the media database Factiva reveal more than 4705 articles related to the words “Libor” and “manipulation”. The search was conducted in May 2015. The selected time period was “01/01/2008–08/05/2015”. Factiva provides a premier collection of the world’s top media outlets, web media, and trade and consumer publications, giving immediate access to thousands of sources in 28 languages from nearly 200 countries. The database contains 35 years of articles, analyst reports and tweets. The top news sources in Factiva include the Wall Street Journal, Dow Jones Newswires, the New York Times, the Sydney Morning Herald, South China Morning Post and Le Monde. See http://new.dowjones.com/factiva-sources/

Abrantes-Metz RM (2012) Why and how should the libor be reformed? Available at SSRN: http://ssrn.com/abstract=2094542 . Accessed 04 Sept 2015

Abrantes-Metz RM, Kraten M, Metz AD et al (2012) Libor manipulation? J Bank Financ 36(1):136–150

Article Google Scholar

Agarwal A, Jain M (2015) Recent development in Libor. Abhinav-National Monthly Refereed J Res Comm Manag 4(3):107–114

Google Scholar

Ashton P, Christophers B (2015) On arbitration, arbitrage and arbitrariness in financial markets and their governance: unpacking LIBOR and the LIBOR scandal. Econ Soc 44(2):188–217

Bank for International Settlements (2013) Towards better reference rate practices: a central bank perspective. Basel

Barclays Plc (2011) Annual Report. London

Barclays Plc (2012) Annual Report. London

Barclays Plc (2013a) Annual Report. London

Barclays Plc (2013b) Barclays’ response to the Salz Review. London

Barclays Plc (2013c) Strategic Report. London

Barclays Plc (2014a) Annual Report. London

Barclays Plc (2014b) Statement on anti-money laundering. London

Barclays Plc (2014c) Strategic Report. London

Barclays Bank Plc (2011) Annual Report. London

Barclays Bank Plc (2012) Annual Report. London

Barclays Bank Plc (2013a) Annual Report. London

Barclays Bank Plc (2013b) Strategic Review. London

Barclays Bank Plc (2014) Annual Report. London

Bonfim D, Kim M (2014) Liquidity risk in banking: is there herding? Available at SSRN: http://ssrn.com/abstract=2163547 . Accessed 04 Sept 2015

Commodity Futures Trading Commission (2012) Order instituting proceedings pursuant to Sections 6(C) and 6(D) of The Commodity Exchange Act, as amended, making findings and imposing remedial sanctions. Washington, DC

Coombs WT, Holladay SJ (eds) (2011) The handbook of crisis communication. Wiley-Blackwell, Oxford

Cui J, In FH, Maharaj EA (2012) What drives the Libor-OIS spread? Evidence from five major currency Libor-OIS spreads. Available at SSRN: http://ssrn.com/abstract=2173944 . Accessed 04 Sept 2015

Dallas L (2012) Short-termism, the financial crisis, and corporate governance. Available at SSRN: http://ssrn.com/abstract=2006556 . Accessed 04 Sept 2015

Financial Conduct Authority (2013) Final Notice 2013: ICAP Europe Ltd. Ref Number 188984. London

Financial Services Authority (2012) Report: Final Notice – FSA. Ref Number 122702. London

Fouquau J, Spieser PK (2015) Statistical evidence about LIBOR manipula tion: a “Sherlock Holmes” investigation. J Bank Financ 50:632–643

Hou D, Skeie DR (2014) LIBOR: origins, economics, crisis, scandal, and reform. Available at SSRN: http://ssrn.com/abstract=2423387 . Accessed 04 Sept 2015

House of Commons Treasury Committee (2012) Fixing LIBOR: some preliminary findings. HC 481–I. London

International Monetary Fund (2008) Global Financial Stability Report. International Monetary Fund, Washington, DC

Keay A (2011) Risk, shareholder pressure and short-termism in financial in stitutions: does enlightened shareholder value offer a panacea? LFMR 5(6):435–448

King TB, Lewis KF (2014) What drives bank funding spreads? Available at SSRN: http://ssrn.com/abstract=2539711 . Accessed 04 Sept 2015

McConnell PJ (2013) Systemic operational risk: the LIBOR manipulation scandal. J Oper Risk 8(3):59–99

Monticini A, Thornton DL (2013) The effect of underreporting on LIBOR rates. J Macroecon 37:345–348

O’Brien J, Gilligan G (eds) (2013) Integrity, risk and accountability in capital markets: regulating culture. Bloomsbury Publishing, London

Rappaport A (2005) The economics of short-term performance obsession. Financ Anal J 61(3):65–79

Rappaport A, Bogle JC (2011) Saving capitalism from short-termism: how to build long-term value and take back our financial future. McGraw Hill Professional, New York, NY

Reputation Institute (2013) UK RepTrakTM Pulse 2013. Forbes

Salz A (2013) The Salz review: an independent review of Barclays’ business practices. London

Download references

Author information

Authors and affiliations.

University Magna Graecia, Catanzaro, Italy

Rosella Carè

You can also search for this author in PubMed Google Scholar

Corresponding author

Correspondence to Rosella Carè .

Editor information

Editors and affiliations.

University of Foggia, Foggia, Italy

Stefano Dell’Atti

Univ. "Magna Graecia" of Catanzaro, Catanzaro, Italy

Annarita Trotta

Rights and permissions

Reprints and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this chapter

Carè, R. (2016). The Libor Case: A Focus on Barclays. In: Dell’Atti, S., Trotta, A. (eds) Managing Reputation in The Banking Industry. Springer, Cham. https://doi.org/10.1007/978-3-319-28256-5_3

Download citation

DOI : https://doi.org/10.1007/978-3-319-28256-5_3

Published : 16 April 2016

Publisher Name : Springer, Cham

Print ISBN : 978-3-319-28254-1

Online ISBN : 978-3-319-28256-5

eBook Packages : Economics and Finance Economics and Finance (R0)

Share this chapter

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

- Publish with us

Policies and ethics

- Find a journal

- Track your research

Updated cookies policy - you'll see this message only once.

Barclays uses cookies on this website. They help us to know a little bit about you and how you use our website, which improves the browsing experience and marketing - both for you and for others. They are stored locally on your computer or mobile device. To accept cookies continue browsing as normal. Or go to the cookies policy for more information and preferences.

Please upgrade your browser

To have the best experience using our site, please upgrade to one of the latest browsers.

An innovation thesis, the first of its kind published by Barclays

The Future of Money, Finance and Banking

12 April 2023

This Innovation Thesis explores the seismic shift financial services is facing and the driving forces behind it, and highlights the themes we consider will prove most relevant in the coming years:

- The Future of Money: Payments 2.0, Digital Money and Beyond

- The Future of Finance: Personalised and Embedded

- The Future of Banking: Harnessing technology to build the bank of the future

The Innovation Thesis has been developed by the Barclays FinTech Venture Studio powered by Rainmaking. Our mission is to ideate, prototype quickly and support to scale innovative new products and services. We do this through collaborations with FinTechs, internal teams and corporate clients.

Subscribe to our weekly newsletter for all the latest FinTech news

Important information

Technology and Operations Management

Mba student perspectives.

- Assignments

- Assignment: RC TOM Challenge 2018

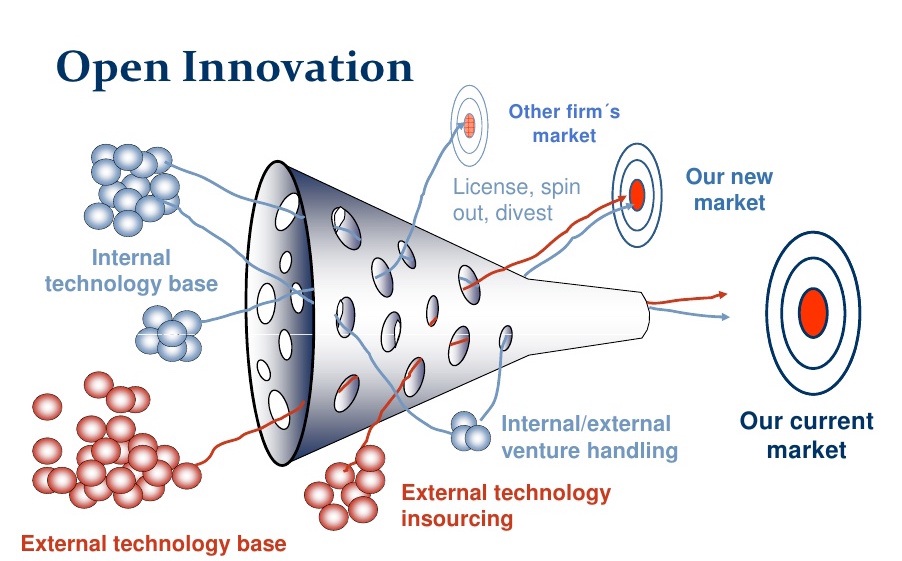

Teaching an Old Bank New Tricks: Open Innovation at Barclays

Who would you trust more for financial advice: 100 randomly selected people or Barclays, a 300-year old bank?

Intuition would say Barclays. However, open innovation – the use of external content and partners in internal product and process development – would contend that the group of 100 could offer some unexpected insights.

Background

Barclays is a large multinational bank offering services from retail banking in the UK to trading. A key driver of its success has been its ability to leverage customer data for products such as credit analytics [2] . This has led Barclays to safeguard customer data and other tools, limiting product development to internal processes only.

However, in the aftermath of the 2007 financial crisis, this strategy became challenged by:

Pathways to Just Digital Future

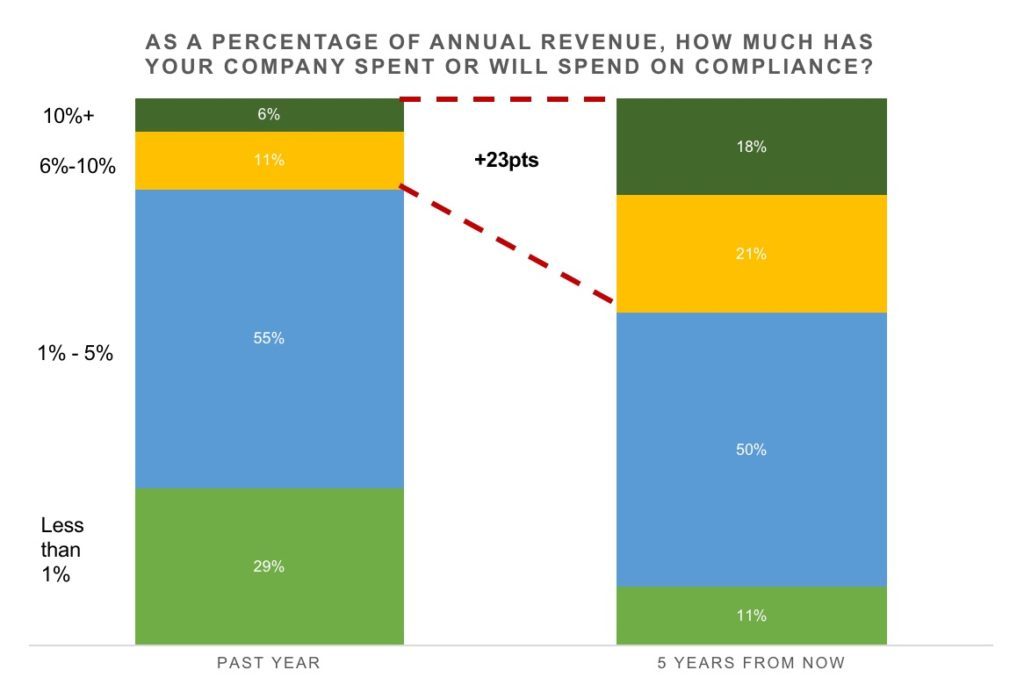

- Constrained resources : The financial crisis and rise of regulation has constrained Barclays’ ability to invest in product development. 40% of Barclay’s IT budget is now spent on compliance [3] (industry trend below).

- Mint: aggregates user data from banks to create budgeting tools

- Vetr: crowdsourced stock research

- Regulation : Open Banking requires UK banks to share customer data with third-parties via APIs [8] .

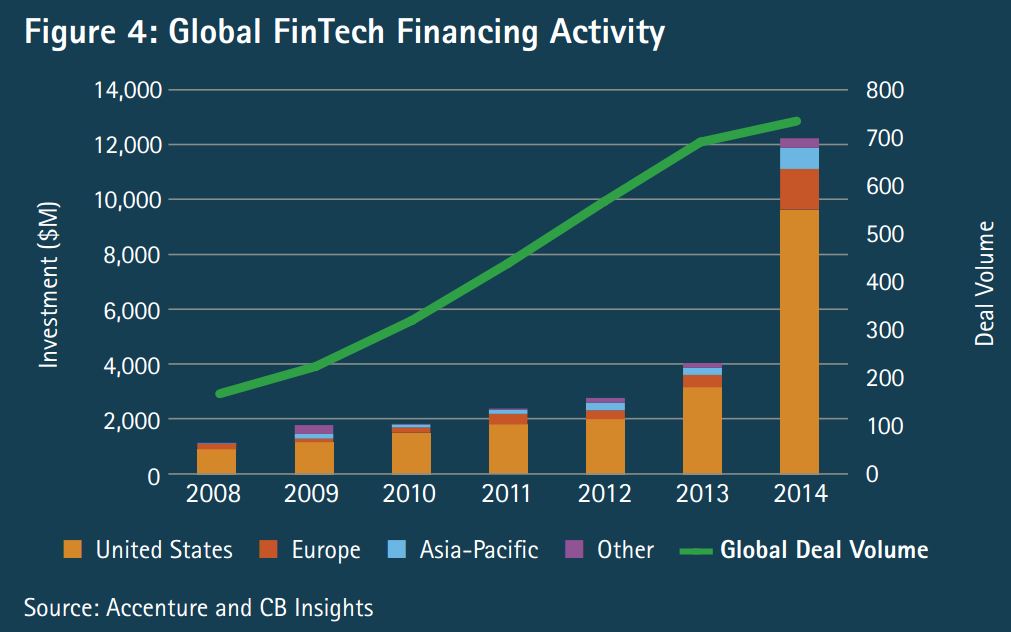

With constrained resources and unfavorable regulatory changes, Barclays’ internal-only product development cannot compete against fintechs’ speed. Consequently, it began to experiment with open innovation as a cheaper, faster, and more expansive form of R&D.

Barclays and Open Innovation – Today

In the short-term, Barclays is addressing the above challenges by using crowdsourcing, an open innovation technique, to develop incremental products and tools:

- Barclaycard Ring Mastercard : Ring is a crowdsourced credit card where customers can propose and vote on changes to the card through a forum. Past votes include removing foreign transaction fee and redesigning the physical card [9] . By crowdsourcing Ring’s features, Barclays was able to customize it to the needs of its customers and increase customer engagement.

- Open source partnerships: Barclays partnered with Australian bank CommScore to release a data extraction tool to the open-source community [10] . This allowed Barclays to replace expensive, proprietary ETLs with a free alternative.

In the medium-term, Barclays is using fintech partnerships to enhance their product development exploration funnel and enable long-term process improvements. Per Magdalena Krön, VP of Open Innovation at Barclays, fintech partnerships are “the new R&D function.” [11]

Barclays engage fintechs through their Accelerator and Rise initiatives. Accelerator provides fintechs with access to Barclays’ technology and network in exchange for equity. Rise are co-working spaces that also host workshops and hackathons. Barclays uses these programs as a funnel to identify and maintain a relationship with high-potential startups (see below), so that Barclays can later launch products by acquiring or partnering with these startups (vs. building in-house). In addition, Rise encourages employees to interact with startups, empowering employees with the skills to “challenge the traditional internal way of doing things [at Barclays].” [11]

Over the next two years, Barclays should incorporate fintech crowdsourcing into their main product line vs. keeping them at arms-length with Accelerator and Rise. Longer term, they should use open innovation to fundamentally change processes within whole functional areas.

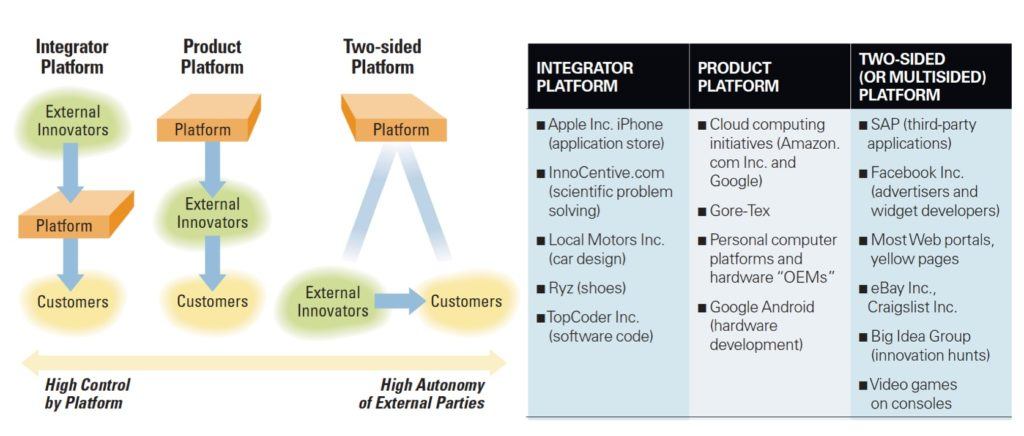

In the short-term, one area of application are the APIs required by Open Banking regulation. Instead of just offering the APIs, Barclays should also create a two-sided platform (see below) available to its customers. Access to Barclays’ wide customer base will encourage third-parties to develop on Barclays platform, which in turn helps Barclays by generating a diverse range of products at lower cost.

More broadly, Barclays should institute a formalized system of crowdsourcing customers for product ideas. 44% of computerized banking services today were first built by a customer [14] . Similar to how software gaming companies use “mods” – alterations made by users to a game – to enhance their core product, Barclays can encourage homemade computerized banking services (e.g., account aggregators, budget tools), potentially via the two-sided platform described above.

In the face of limited resources and increasing competition and regulation, Barclays has experimented with crowdsourcing and fintech partnerships. Early success of these open innovation programs suggest that Barclays should consider further embedding open innovation into their core products and services instead of ring-fencing them.

Nevertheless, key questions remain as to the effectiveness and unintended consequences of using open innovation in banking, including:

- Does open innovation increase Barclays’ risks of commoditization and disintermediation?

- How should Barclays maintain controls and cybersecurity within an open innovation ecosystem?

(794 words)

[1] Chesbrough, H. (2004). Open Innovation: Renewing Growth from Industrial R&D. In 10th Annual Innovation Convergence . Minneapolis.

[2] Gohman, K. (2018). Open Banking: What U.S. Banks Need To Watch. Retrieved from https://www.forbes.com/sites/forbesfinancecouncil/2018/03/15/open-banking-what-u-s-banks-need-to-watch/#65dc828d2af9

[3] Riley, J. (2018). Compliance projects take 40% of Barclays Bank’s IT budget. Retrieved from https://www.computerweekly.com/feature/Compliance-projects-take-40-of-Barclays-Banks-IT-budget-says-technology-chief

[4] Korek, J. (2018). Global Regulatory Outlook 2018 . Duff & Phelps. Retrieved from https://www.duffandphelps.com/-/media/assets/pdfs/publications/compliance-and-regulatory-consulting/global-regulatory-outlook-2018.ashx?la=en

[5] Fintechs stand for Financial Technology firms. In general, fintechs refer to non-bank startups.

[6] Hardie, S., Wood, J., & Gee, D. (2018). Innovation, Distributed: Mapping the fintech bridge in the open source era [Ebook]. MagnaCarta Communications, ACI. Retrieved from https://www.aciworldwide.com/-/media/files/collateral/other/aci-magna-carta-fintech-disruptors-report.pdf

[7] Accenture. (2018). The Future of FinTech and Banking: Global Fin Tech Investment Triples In 2014. Retrieved from https://www.cbinsights.com/research/fintech-and-banking-accenture/

[8] APIs are protocols for how software components should interact and talk with each other.

[9] Harkness, B. (2018). 2018 Review: Barclaycard Ring Mastercard – Most Unique Credit Card?. Retrieved from https://www.creditcardinsider.com/reviews/barclaycard-ring-mastercard-review/#the-ring-community

[10] Tony Kerrison – Head of Infrastructure Services, Barclays bank PLC (2017). . San Francisco: Boardroom Insiders, Inc. Retrieved from http://search.proquest.com.ezp-prod1.hul.harvard.edu/docview/1891116054?accountid=11311

[11] How Barclays is waking up to open innovation | Barclays. (2018). Retrieved from https://www.home.barclays/news/2016/11/northern-light–magdalena-kroen-talks-fintech–innovation-and-ge.html

[12] Rose, L. (2018). “Barclays Accelerator: Tel Aviv 2017”. Retrieved from https://www.slideshare.net/Dataconomy/barclays-accelerator-liron-rose-managing-director-at-tech-stars-tel-aviv

[13] Boudreau, K., & Lakhani, K. (2018). How to Manage Outside Innovation. MIT Sloan Management Review , Summer 2009 , 69-76.

[14] Oliveira, P., & von Hippel, E. (2011). Users as service innovators: The case of banking services. Research Policy, 40 (6), 806. Retrieved from http://search.proquest.com.ezp-prod1.hul.harvard.edu/docview/871974573?accountid=11311

Student comments on Teaching an Old Bank New Tricks: Open Innovation at Barclays

Hi Annie, Great job on a thorough and well-structured essay. I liked the graphs and examples of recent successes. In terms of how these startups can impact the bottom line at Barclays, I am curious about which use cases or topics need to be prioritized. My takeaway is that all companies should look at instituting the “mod” model to crowdsource product enhancements from their customers.

It is fascinating to hear how a “large old” bank is doing its best to stay young and with the times. I couldn’t help but think about the opening comment and how consumers don’t trust big banks for financial advice. The majority of Americans are considered financially illiterate and the nation is in desperate need of an improvement in financial education. It seems that the community the bank created could help them find ways to better encourage customers to educate themselves or providing them with a platform to learn basic financial principles. Ultimately they run the risk of losing customers but should create new products or services to help customers improve their financial lives.

This article leaves me wondering what kind of bias a company might face when using open innovation and how reliable that information will be about their customer base. For the Vetr example you used, I can imagine that the crowd sourced data set might be overly bias towards the technology sector due to the nature of it being a web-based platform. For the Barclaycard Ring Mastercard, I would question if the voting mechanism accurately represents the cardholder’s interests. There are ways to ensure that open innovation is coming from the target customer. The best example of this done right is the one you provided about gaming mods. This is a bottom up approach driven by early adopters and high frequency gamers that drive the industry trends. If Barclays can ensure that their open innovation data is not biased and are aware of the specific customer base that is contributing the majority of the information, then I agree that it will be a competitive advantage for the bank.

I really liked this article–thanks for sharing! I am impressed by the Ring product and how Barclays uses the forum to incorporate customer feedback into product development. I am curious to know whether the feedback/conversation is one- or two-sided. E.g., does Barclays communicate to the Ring community the trade-offs that they may have to face as they add new features to the card, or is that communicated via the fees and features of the next release of the product? I love the idea of crowdsourcing customer service. I see this done by Apple a lot; the Apple forums provide great answers to all of my Apple tech questions. It’s great to see big banks working to be more innovative–would love to see more of this!

This is a very interesting application of crowdsourcing. Something I was left wondering is how this might impact them in terms of competitors. If other (similar) banks begin to use the same process to drive product innovation, how would Barclays ensure a competitive advantage? By this I mean, if product innovation is coming from crowdsourced ideas, what would stop other banks from getting the same ideas from customers?

I loved your suggestion for creating a two-sided platform and crowdsourcing in customer service! They are brilliant ideas that would make the “old institutes” adapt to the new era better. I agree that open source will help with the product development cycle but definitely will also bring down the quality and controls Barclays maintained in the past. On a separate note, it was great to know that Barclays was able to customize based on customer feedbacks and increase customer engagement. But who are they going to listen to, the louder one or the less profitable to bank one? I see a conflict of interest in an openly designed banking product.

Leave a comment Cancel reply

You must be logged in to post a comment.

Barclays uses cookies on this website. Some cookies are essential to provide our services to you. Other cookies help us to analyse how you use the site, so we can improve your experience on our site. Cookies are stored locally on your computer or mobile device. Please select 'Accept all' to consent to cookies or select ‘Reject all’ to reject all but essential cookies or select 'Manage cookies' to change your preferences. For more information visit our cookie policy .

- Private Bank

- Our Insights

Investing for Global Impact

How will you influence tomorrow?

The global shift towards sustainable investing continues at pace, and it’s a megatrend that continues to grab attention and spark debate. Investors are increasingly recognising the opportunities for both purpose and profit, as well as the importance of managing sustainability risks in their portfolios.

Faced with a climate emergency, mounting social challenges and the fallout of the pandemic, more investors are feeling the responsibility to shape a brighter future for the generations to come.

'Investing for Global Impact: A Power for Good' report

We’re delighted to unveil the ninth edition of the ‘Investing for Global Impact: A Power for Good’ report. Developed by Campden Wealth, in partnership with Barclays Private Bank and Global Impact Solutions Today (GIST), it provides unique insights into the attitudes and actions of some of the world’s wealthiest individuals, families, family offices and foundations towards generating positive impact with their capital.

The latest report surveyed nearly 150 UHNW investors, with an average portfolio of $730 million, and reveals why and how they’re investing sustainably, and where the hurdles lie. It’s a thought-provoking read for anyone interested in investing for impact, irrespective of experience.

The need for change has never been greater. Are you rising to the challenge?

Six sustainable investing insights from UHNW investors

We highlight key takeaways from this year’s report and explore their potential relevance for your own portfolio.

Aligning family philanthropy and investing for impact

Looking to increase your positive impact on the world? Read how some wealthy families use their capital to influence a better tomorrow.

Podcast: Philanthropy and impactful investing

Tune in as Juliet Agnew and Damian Payiatakis discuss philanthropy and investing, and how families and foundations are joining the dots between the two.

How to start your journey to a greener investment portfolio

As the global climate emergency intensifies, the first of our updated three-part series explores how you can establish your goals for a greener portfolio.

How to turn climate ambition into portfolio action

Private investors’ capital can play a critical role in addressing climate change. Here we discuss translating your climate ambitions into tangible investor action.

How to manage your portfolio’s climate impact

How well are your investments delivering on your climate ambitions? Discover how to measure, assess and improve climate risks and opportunities in your portfolio.

Our transition to net zero

We believe that Barclays can make a significant contribution to tackling climate change and help accelerate the transition to a low-carbon economy. Read more about how we’re realising our ambition to become a net-zero bank by 2050.

Download the ‘Investing for Global Impact’ report

Unique insights into the motivations and experiences of UHNW individuals, families, family offices and foundations when it comes to investing sustainably.

Disclaimer This communication is general in nature and provided for information/educational purposes only. It does not take into account any specific investment objectives, the financial situation or particular needs of any particular person. It not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful for them to access.

This communication has been prepared by Barclays Private Bank (Barclays) and references to Barclays includes any entity within the Barclays group of companies.

This communication:

(i) is not research nor a product of the Barclays Research department. Any views expressed in these materials may differ from those of the Barclays Research department. All opinions and estimates are given as of the date of the materials and are subject to change. Barclays is not obliged to inform recipients of these materials of any change to such opinions or estimates;

(ii) is not an offer, an invitation or a recommendation to enter into any product or service and does not constitute a solicitation to buy or sell securities, investment advice or a personal recommendation;

(iii) is confidential and no part may be reproduced, distributed or transmitted without the prior written permission of Barclays; and

(iv) has not been reviewed or approved by any regulatory authority.

Any past or simulated past performance including back-testing, modelling or scenario analysis, or future projections contained in this communication is no indication as to future performance. No representation is made as to the accuracy of the assumptions made in this communication, or completeness of, any modelling, scenario analysis or back-testing. The value of any investment may also fluctuate as a result of market changes.

Where information in this communication has been obtained from third party sources, we believe those sources to be reliable but we do not guarantee the information’s accuracy and you should note that it may be incomplete or condensed.

Neither Barclays nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation.

Important information

Academia.edu no longer supports Internet Explorer.

To browse Academia.edu and the wider internet faster and more securely, please take a few seconds to upgrade your browser .

Enter the email address you signed up with and we'll email you a reset link.

- We're Hiring!

- Help Center

DIGITALIZATION OF THE FINANCIAL SECTOR AND CHANGE MANAGEMENT OF BARCLAYS BANK

ABSTRACT Rapid technological changes and digitization have an impact on the performance of various sectors. The main purpose of this research study is to evaluate the impacts of digitization of Barclays bank and how the change management strategies have affected the employees. In essence the study was focused on determining the perspectives of employees regarding the handling of digital changes at the firm. In order to achieve these objectives the study relied on the use of questionnaires which were administered using email. Up to 163 participants took part in the study. The results from the questionnaires in this case enabled the questionnaire to complete the study. The study revealed that a large fraction of the employees are contented with the change management strategies which have been put in place at the firm. Some of the reasons given for the support included the indication that digitization has had a positive impact on their professions. The positive response was a reflection of an effective change management strategy at Barclays. The study recommends that the firm should put in place measures to ensure that the other employees who oppose the changes are well educated regarding the benefits of the changes and that proper communication system is put in place.

Related Papers

Sustainability

Florian Diener

The digitalisation of banks is seen as the omnipresent challenge which the banking industry is currently facing. In this digital change process, banks are facing disruptive innovation that requires adaptation of almost all cooperative processes. Digital transformation in the financial industry is associated with obstacles that seem to hinder smooth implementation of digital approaches. This issue has not been adequately addressed in the current academic literature. The main purpose of this qualitative exploratory study is to identify the main perceived obstacles to digital transformation in both the private and commercial banking sectors from a managerial point of view and to analyse them accordingly. The methodology is based on a methodological approach using a combination of contextual interviews with German board members of banks, inductive content analysis, and the exploration of best-practice approaches. The findings revealed that elements of strategy and management, technology...

IOSR Journals

Purpose: The purpose of this study is to analyse and understand the scope of digitalization and its impact on employee performance in banking sector. Method: The paper is based on a qualitative approach and structure was designed based on semi-structured interviews conducted via telephonic calls with employees from select banks to enable connections between theories and pragmatic findings. Findings: After analyzing the data very efficiently, found that digitalization has significantly impacted the employee performance in the banking sector. It has become a facilitator by being a platform for the employees to perform their tasks efficiently. Further, as digitalization develops, managers have been using strategies like advanced support systems, fast and transparent communication methods, and different digital tools to bring up employees' performance at work. Therefore, digitalization positively affects employee performance in most instances, but managers can not overlook the possibilities of negative implications too.

Journal of Business Administration Research

Hanen Khanchel

In this paper, we discuss in more detail the context of Tunisian banks, with a focus on digital transformation strategies considered, the mission that preceded this study and the methodology and approach. Secondly, we will analyze the results of the study to reconstruct the features of the digital transformation of movement in Tunisian banks.The study of the digital transformation of Tunisian banks is carried on the board Matine Consulting firm. This study is launched in the continuity of the inaugural training program certifying on the topic of FinTechs and digital transformation of banks, set up by Matine in collaboration with the Academy of Banking and Finance (ABF).

Natasa Krstic

Journal of Open Innovation: Technology, Market, and Complexity

Fotis Kitsios

Digital transformation in the banking sector is a continuous process that affects both the external and internal environment by redesigning internal processes and existing methods. There are many reasons that digital transformation takes place, such as servicing remote areas without physical branches, differentiation from competitors or reduction of operating costs. In any case, there are a lot of doubts about the acceptance of digital technologies. Thus, this article examines the acceptance rate of digital transformation in the banking sector in Greece. One hundred and sixty-one employees at Greek banks completed the survey. A Multivariate Regression Analysis was implemented to analyze the items of the Technology Acceptance Model. The findings of this paper indicate the perception of bank employees with regard to new technologies. This paper provides a practical contribution for executives of Greek banking organizations to schedule targeted educational programs to facilitate the tr...

Harsh shrimali

Journal of Insurance and Financial Management

[JIFM] Journal of Insurance and Financial Management

The purpose of this study is to evaluate the results on the challenges facing universal banks in a digital world. The study is based on a survey of more than 100 leading German and Swiss banks as well as management consultancies. The current business model of universal banks is obsolete. New technologies, increasing internet use and changing customer behavior, are leading to the emergence of new business fields. FinTech are the drivers of financial innovation. The universal banks cooperate with fintech in various forms. The banks are facing hurdles to digitize their business.

International Journal of Management Studies

Thanga Helina 2130

IAEME PUBLICATION

IAEME Publication

Since the beginning of the 21st century, a new phenomenon has emerged in several aspects of our society: the digitalization. People could suppose that digital transformation is only about tech-savvy industries but in reality; it concerns all conventional businesses. While affecting almost all kinds of business and their managerial practices, the digitalization somehow forces not to implement several traditional practices which are considered to be the Holy book for managers. The leadership community should need to accept and follow the non-traditional steps for emerging new innovations and experiment in new managers. The purpose of this thesis is to explore and identify how the managers and their practices are affected by digitalization. The new era of digital transformation has already taken up the globe in the recent times of coronavirus. This digitalization has provided and influenced the managerial aspects which mainly has turned the school of thought for the majority of managers. The purpose of study is to explore how managers practices are transforming in this era of digitalisation. This study concluded notable and variant changes in managerial practices, as it shows that digitalization is the process which transforms the task of managers. The tasks include both by aiding the managers and creating a difficulty to some extent towards their responsibilities and area of domain. Thus it highlights the managers to be adaptive and more aware of the changes that are bought up by digitalization to their practices..

Technology audit and production reserves

Natalia Babko

The article analyzes the current problems of the financial sector within the framework digital transformation and the gradual transition to digital service financial transactions. The object of research is the Ukrainian financial banking sector, the peculiarities of which functioning at this stage crisis economy Ukraine require finding adaptation ways for the introduction digital transformation procedures. The subject is financial relations in the digital adaptation sphere and innovative development banking through the prism involvement of tools and information technologies in financial system, in general, and financial operations and procedures, in particular. The problems domestic financial sector transformation became more acute in connection with the mass transition to remote channels interaction with clients, first due to the restrictions that were applied as a result the COVID-19 pandemic, and then due to the armed aggression of russia to Ukraine. The research methodology is b...

Loading Preview

Sorry, preview is currently unavailable. You can download the paper by clicking the button above.

RELATED PAPERS

Risk in Contemporary Economy

Disruptive Technology and Digital Transformation for Business and Government

Fatmanur Deniz

Lawand Bahram

Information Resources Management Journal

TENDESAI CHINAMASA

Test Engineering And Management

SHAKEB AKHTAR , Shujaat Azmi

Jurnal Ad'ministrare

riris shanti

Finiz, Singidunum University International Scientific Conference

Vesna Martin, Ph.D.

Digitalisierung – „the next challenge“ für Sparkassen Handlungsfelder zur künftigen Gestaltung des Geschäftsmodells in Sparkassen

Piotr Komorowski

Journal of General Management

Ioannis Krasonikolakis

IJRMS Journal

International Journal of Multidisciplinary Research and Analysis

Harjoni Desky

Lova Ravalimanana

Dan-jumbo Idaerefagha

Rathi Meena

James Njenga

Sailesh Sewpaul

International Journal of Marketing Studies

George Konteos

Dr Sudhinder Singh Chowhan

Leeds University Business School

Priyanka Sharma Gupta

Soulef Smaoui

soulef smaoui , Mohemmad Manawer Mikhlif

Management and Labour Studies

Anshu Yadav

Indus Foundation International Journals UGC Approved

Market Infrastructure

Natalia Shyriaieva

- We're Hiring!

- Help Center

- Find new research papers in:

- Health Sciences

- Earth Sciences

- Cognitive Science

- Mathematics

- Computer Science

- Academia ©2024

For more information contact

[email protected], equity research.

Event analysis and deep dives into stock ideas and sector themes spanning more than 1,700 companies under coverage across the Americas and Europe.

For more information contact [email protected]

Our Product Mix

Single stock.

Full Signal

Our brand for in-depth fundamental single stock research

#futureofmedia

Our brand for in-depth fundamental single stock reseaTracking the most relevant market themes

UK Mid & Small Cap

Market-leading directory spanning 245 UK stocks

Transatlantic

Transatlantic Collaboration

A fresh perspective on today’s global sectors

Analyst Coverage (as of 19 June 2017)

- Building & Building Products

- European Payments & Fintech Forum

- European Retail Forum

- CEO Energy-Power

- Global Consumer Staples

- Global Financial Services

- Global Financial Services Global Automotive

- Global Technology, Media and Telecommunications (TMT)

- Industrial Select

- Global Healthcare

Equity Industries Under Coverage

(as of 28 June 2017)

Size of the bubble denotes total market capitalization of our coverage stocks in each industry.

Company Pages

Access company research, upside/downside scenario ranges and company financials, including three-year forecasts across income statement, balance sheet and cashflow.

Barclays Equity Research’s "Top Picks" represent the single best alpha-generating investment idea within each industry, taken from among the Overweight-rated stocks within that industry.

Managers in the Barclays Bank Research Paper

- To find inspiration for your paper and overcome writer’s block

- As a source of information (ensure proper referencing)

- As a template for you assignment

Introduction

Bass’ theory of leadership, problems facing leadership, solutions to resistance to change.

An individual can construe the word organization in many ways. In this paper, two definitions will be provided. One of the meanings is related to human organization and the other is linked to material organization. An organization is defined within the context of business meaning that without commerce, an organization would not exit. Barclays is purely a commercial and financial organization.

The word business is defined as human economic action. It entails permanent and standard manufacture and allocation of goods and services with an aim of making a profit. Currency streaming in and acquisition of income through fulfilling the needs of customers are the two methods of assessing the strengths of Barclays Bank.

Furthermore, business organization is a procedure or an art of instituting effectual collaboration between the factors of production such as land, material, asset equipment and personnel for generating or obtaining capital with an aim of earning profit in a business venture.

The scope of business organization has significantly extended after the industrial revolution. The process of manufacturing is now intricate. An organization is required to establish what each individual will do and how much power each will have. At this level, an organization is mostly divided into three categories based on business ownership.

These categories are solitary proprietorship, joint venture and corporation. Barclays Bank is a Multinational Corporation trading in a number of states. The organization assists owners to use factors of production competently and hence condense the cost of production.

This facilitates realization of organizational ambitions and goals at a least cost. An excellent organization enables optimal utilization of scientific advancements to create support. Barclays Bank resolves all the advertising tasks such as buying, selling, shipping, warehousing, funding, and product regularity through setting up tasks to each person.

Organizational stakeholders in Barclays Bank include the management, employees, shareholders, clients, customers and the community. The top executive is supposed to coordinate the activities of the organization by ensuring that each person’s wishes and desires are identified and fulfilled (McCluskey, 2004). As leaders of the Bank, managers must treat employees courteously and involve them in decision- making processes.

This article addresses the issue of organization in a business environment and how it shapes other factors as well as how other factors shape it. The paper goes ahead to discuss the concept of leadership since it is established as one of the critical aspects. The paper uses the management system of Barclays as an example. An organization cannot excel without leaders who are full of visions.

Specifically, the paper identifies resistance to change as being one of the factors affecting leadership in Barclays Bank. Many factors make workers to resist change, which are discussed in this paper. Finally, the paper concludes after discussing some solutions to resistance to change.

It is true that excellent leaders are made not born meaning that any person could become an effective leader provided he/she has the desire and willpower. High-quality leaders develop through a never-ending procedure of self-study, edification, schooling and familiarity. For a leader to achieve his or her dreams, there are three things that must be understood deeply.

The first one is developing some qualities implying that a manager must be someone who is reliable and effective. Again, an individual has to conduct some research to know exactly what he/she is required to do. Finally, a good manager must go ahead and executive the roles or responsibilities assigned to him/her. In short, the three things to be mastered in leadership are ‘be’,’ know’ and ‘do’.

These factors are not acquired logically but are obtain through regular work and research. Excellent leaders are ceaselessly working and learning to advance their management talents. This means that good leaders do not rest on their success.

In the modern managerial front, there are four factors of leadership, which include a leader him/herself, followers, communication and situation. As a leader, an individual must have an honest understanding as regards to who he/she is. This is determined through knowing one’s capacities and limitations. Stakeholders are to judge the success of a leader not otherwise.

Leaders with low self-esteem can negatively inspire employees leading to poor performance in the organization. Therefore, a leader can only be successful if he/she manages to convince workers. On the part of followers, a leader needs to identify the various techniques of supervision to be applied in guiding employees. For instance, new employees are not to be supervised in the same way as the experienced ones.

Some employees are highly motivated while others are not, hence the leader must consider this aspect. A good leader must know his/her people by understanding their nature such as feelings, desires and enthusiasm. In an organization, leaders need to embrace interpersonal communication, which should be in form of non-verbal. The way a leader addresses his/her junior employees affect production in the organization.

For this reason, a leader must set an example by embracing the most efficient communication model. Furthermore, leaders need to acknowledge diversity and appreciate the fact that not all situations are the same. In this case, a leader needs to possess tact and special skill to be able to differentiate problems.

Each problem has a unique feature meaning that solutions are also different. In this sense, a leader should be well placed and timely in order to identify the correct time of confronting an employee. Scholars of management suggest that leaders should utilize Process Theory to solve employee problems other than utilizing trait theory (Montana, & Bruce, 2008).

The theory elucidates that there are three major techniques of describing how individuals turn out to be leaders. The theory focuses more on the group implying that it analyzes relationships between small groups of people in the organization. The theory starts by postulating that people posses some special traits that may give them chances to be leaders.

This statement concurs with the findings of trait theory. In this regard, an individual can conclude that leaders are born because the characteristics are intrinsic. The theory posits further that a particular event may force an individual to rise up to an occasion and show leadership. Leadership qualities may crop up during hard times such as calamities, natural disasters or crises.

An event may force an individual to demonstrate extraordinary leadership qualities. These findings are in line with the postulations of Great Events Theory. Bass’ theory of leadership continues to emphasize that people can decide to be leaders, meaning that they can learn leadership skills (Spillane, & Diamond, 2004).

The recent theory referred to as Transformational or process theory supports these findings. Furthermore, it is the most treasured theory. In fact, this paper utilizes the findings of the theory in analyzing major leadership problems.

In the previous chapter, change was identified as the major problem facing leadership in the organization. In this section, some reasons that make people to resist change will be explored. The risk of change is seen by some stakeholders as being superior to the danger of standing still. This means that initiating change calls for determination and faith.

Change means that an organization decides to move in a different direction, which is highly unpredictable. Organizational leaders only anticipate for success but there is no surety. In an organization, people will only accept to abandon their traditional ways of doing things if the conditions prevailing are unbearable. This is usually viewed as one way of managing risk.

Policy makers in an organization are therefore requested to be truthful and prove that change will improve the working conditions in the organization. Furthermore, change agents in the organization are urged to be rational and avoid unrealistic and concealed promises of rewards. Upon evaluation of risk, the power of human flight reaction is stimulated to fight for change.

In the organization, people seem to be connected to some individuals who are identified with old techniques. Because human beings are social species, they have a liking of remaining where they are for a long time. Employees have a tendency of following those who taught them how to carry out duties in the organization. Loyalty therefore becomes one of the reasons why people resist change.

Suggesting some new ways of executing duties means going against the wishes of the old guard, who have a large following in the organization. People would not consider the rationality of the idea mainly because of emotional connection to those who taught them (Hewlett, 2006). Change agent should honor the achievements of the old guard before introducing anything new.

On a different note, people tend to resist new techniques because they do not have role models. For that reason, change agents should never underestimate the power of observational learning. Individuals advocating for change in the organization are likened to a dreamer, who employ the power of imagination to formulate new possibilities that are currently non-existent.

It reaches an extent where communication alone would not solve the problem. This implies that change advocates must get some individuals on board and explain to them how new techniques or methods work. Such people will in turn come in handy when it comes to explaining the new idea to others.

This would require the advocates to conduct a pilot study, whereby the new knowledge is tested using a small sample of employees in the bank. Closely related to the above point is the issue of competence. People fear that they possess little knowledge as regards to the new idea or technique.

To such individuals, change means loss of jobs. In this situation, change agents should motivate individuals effectively. Even more, a victorious change crusade consists of successful new training plans, characteristically staged from extensive objectives to more specific.

By this, it implies that preliminary measures should present the validity and preparation for change, state next stages, demarcate future interaction channels and state how people will learn the particulars of what they will be required to do. Afterward, training plans must be executed and assessed ultimately.

Thus, change agent can reduce the initial fear of lack of individual capability for change by demonstrating how individuals will be brought to fitness all through the change process.

People expect a loss of status or value of life because of introducing new ideas. Actual change reallocates duties to individuals. Reorganization of the human resources can bring victors and losers. Some individuals would probably be promoted while others may lose their jobs. Change is not necessarily a zero sum game meaning that it can bring more benefits to individuals than expected.

Some individuals would be aligned against change since they will obviously, and in some incidences appropriately, perceive change as opposing their desires and wishes. There are several tactics for reducing this and for tackling persistent barriers to change in the form of individuals and their safety. This would include helping individuals to adjust accordingly.

Change must not favor one person in the organization. Others will of course benefit while others will loss terribly. Irrespective of what happens, organizational objectives and goals are more important. Leaders should understand this and move on with their plans of introducing change. The aim of leaders is to stabilize the financial base of the organization, not fulfilling individual interests.

Before proposing any project, change agents must explain to stakeholders how the new knowledge will be executed and what could be the possible advantages and disadvantages. This implies that workers and relevant stakeholders should be taken through training sessions to sharpen their wits as regards to new ideas. Leaders need to come up with ways of influencing the attitudes of stakeholders.

Change will only be accepted in the organization if the interests of all individuals are taken care of. On the other hand, change should not be transferred from one place to another without considering environmental and cultural factors. Ideas generated in Europe could not suit the African environment. Techniques and methods imported from other parts need to be reviewed and modified to suit local expectations.

Finally, change should be introduced in stages in order to allow individuals to adjust accordingly (Tittemore, 2003). New methods can be mastered with time instead of rushing people to learn them quickly. Therefore, Barclays must not force its subsidiaries in the developing world to copy western organizational cultures. Each country has its own laws, which vary from one country to another.

Leadership plays a critical role in organizational management. The organization cannot do without good leaders. The success of Barclays bank is attributed to its excellent managers who have superior leadership qualities. Managers in the bank have frequently utilized process theory of leadership to solve managerial problems. The theory suggests that leaders are both born and made.

This implies that an individual can become a competent leader through education. The bank experiences one major problem that is related to adjustment to change. The old guard is against introduction of new managerial techniques. They fear that new methods could render them jobless. Leadership is an important aspect in the organization implying that each manager must strive to achieve it.

Implementation of new policies needs careful review. Rushing workers through changes would cause more problems in the organization. Consultation and proper communication of ideas enables effective implementation of new ideas and techniques.

It is the role of managers to learn the mood of workers and other stakeholders and come up with sufficient techniques of solving their concerns. Self-interest is one of the factors that demoralize change agents in the organization. Other theories that talk about leadership can be used jointly with the process theory to explain leadership in the organization effectively.

Hewlett, R. (2006). The Cognitive leader . New York, NY: Rowman & Littlefield.

McCluskey, M. (2004). How Mature is Your Service Operation?” Supply Chain Management Review , 8(5).

Montana, J., & Bruce, H. (2008). Management Hauppauge . New York, NY: Barron’s Educational Series.

Spillane, J., & Diamond, J. (2004). Towards a theory of leadership practice. Journal of Curriculum Studies, 36(1).

Tittemore, J.A. (2003), Leadership at all Levels . Toronto: Boskwa Publishing.

- Employee Selection Strategies

- Olympic Delivery Authority (ODA) sustainable development

- Adopting Agile Practices in Barclays Company

- Barclays Bank CSR

- Factors Which Impact Barclays Bank

- Organizational Training Design

- Healthcare Facility Knowledge Management Solutions

- Labor Market in Corporations

- Quality management

- Impact of the Cultural Attributes on Management in Muslims

- Chicago (A-D)

- Chicago (N-B)

IvyPanda. (2019, May 17). Managers in the Barclays Bank. https://ivypanda.com/essays/managers-in-the-barclays-bank-research-paper/

"Managers in the Barclays Bank." IvyPanda , 17 May 2019, ivypanda.com/essays/managers-in-the-barclays-bank-research-paper/.

IvyPanda . (2019) 'Managers in the Barclays Bank'. 17 May.

IvyPanda . 2019. "Managers in the Barclays Bank." May 17, 2019. https://ivypanda.com/essays/managers-in-the-barclays-bank-research-paper/.

1. IvyPanda . "Managers in the Barclays Bank." May 17, 2019. https://ivypanda.com/essays/managers-in-the-barclays-bank-research-paper/.

Bibliography

IvyPanda . "Managers in the Barclays Bank." May 17, 2019. https://ivypanda.com/essays/managers-in-the-barclays-bank-research-paper/.

- Overall Rating

Barclays Pros and Cons

- About Barclays Bank

- Interest Rates and Fees

- Digital and Mobile Banking

- Customer Service and Support

Barclays FAQs

- Savings Account Review

- Credit Cards Review

- Personal Loans Review

How Barclays Compares

- Why You Should Trust Us

Barclays Bank Review 2024

Affiliate links for the products on this page are from partners that compensate us and terms apply to offers listed (see our advertiser disclosure with our list of partners for more details). However, our opinions are our own. See how we rate banking products to write unbiased product reviews.

The bottom line: Business Insider's personal finance team compared Barclays to the best online banks and decided that most of its banking products and services — with the exception of its CDs — are on par with other online institutions, and don't particularly stand out.

The bank is still a good choice if you're specifically interested in opening a CD online — it pays some of the best CD rates for accounts with $0 minimum opening deposits.

| Account Type | Annual Percentage Yield (APY) |

| 4.35% | |

| up to 4.80% | |

| 4.85% | |

| 5.10% | |

| 4.85% | |

| 4.50% | |

| 4.00% | |

| 3.50% | |

| 3.50% | |

| 3.75% |

Barclays Bank Overall Rating

| Feature | Business Insider rating (out of 5) |

| Savings accounts | 4.25 |

| CDs | 4 |

| Trustworthiness | 4.5 |

| Total | 4.25 |

About Barclays

Barclays is an online bank. In the U.S., it has high-yield savings account and CDs. The bank also offers personal loans by invitation only, and co-branded credit cards with companies like Jet Blue and Gap. It doesn't have any credit cards for its own brand, though.

Barclays does not offer a checking account , so depositing or withdrawing cash quickly is difficult with Barclays. You'll have to transfer or deposit funds to an external bank account, which can be tedious.

Barclays bank accounts are protected. Your deposits are insured by the FDIC for $250,000, or $500,000 for joint accounts.

Is Barclays Trustworthy?

The Better Business Bureau gives Barclays an A+ rating . A strong BBB rating signifies the company is transparent in how it handles business, responds effectively to customer complaints, and is honest in its advertising.

In 2022, Barclays paid $361 million in a settlement with the U.S. Securities and Exchange Commission. The SEC claimed the bank distributed a high number of unregistered securities and didn't thoroughly keep track of security sales. Although Barclays settled, the bank neither confirmed nor denied these charges.

Barclays Interest Rates and Fees

Barclays interest rates on savings accounts and cds.

Like other online banks, Barclays savings and CD rates are higher than average bank account interest rates . Online banks tend to offer better rates than brick-and-mortar banks because they have fewer overhead costs.

If you compare the bank's savings accounts to competition from other online banks these accounts fall somewhere in the middle. The Barclays Online Savings Account has a lower APY than the best high-yield savings accounts , but similar rates to other national brands.

Meanwhile, Barclays Tiered Savings offers the potential to earn more interest than the Barclays Online Savings Account , but it has a high minimum balance requirement to earn its best rate. A few of our top picks for high-yield savings accounts have a comparable APY to Barclays Tiered Savings but lower minimum balance requirements to earn interest or none at all.

Barclays CDs stand out because they pay competitive rates compared to other institutions with similar opening criteria.

Barclays Fees and Charges

Barclays doesn't charge monthly bank maintenance fees on its savings accounts. For CDs, you'll only face a charge if you withdraw money before your term fully matures. Online banks tend to be a good option for minimal bank fees, as many won't charge high fees.

Barclays Digital and Mobile Banking

Consider other banks if you value having a strong mobile app. Barclays has mediocre ratings overall — it's received 1.9 out of 5 stars in the Google Play store and 3.2 out of 5 stars in the Apple store. Other banks also have more customer reviews.

Barclays Mobile App Features

While the Barclays mobile app doesn't have the best ratings, it does offer most standard mobile banking features. With the mobile app, you can check your transaction history, make mobile check deposits , and transfer money to external bank accounts.

Barclays Online Banking Tools

You can also log into the Barclay's website to manage your accounts. Furthermore, the website has a CD calculator to determine potential interest earnings and another tool to help you set a timeframe for your savings goal if you have Barclays Tiered Savings or the Barclays Online Savings Account .

Barclays Customer Service and Support

You can talk to Barclays customer service is by phone or live chat seven days per week. Contact a representative anytime from 8 a.m. to 8 p.m. ET.

Barclays Bank offers savings accounts, CDs, and co-branded credit cards. People who get an invitation code can also apply for personal loans.

The Barclays Online Savings Account pays 4.35% APY, and Barclays Tiered Savings pays up to 4.80% APY. Barclays CDs pay 3.50% to 5.10% APY, and the rate depends on the term.

You can contact Barclays Bank customer service by phone or live chat.

The pros of banking with Barclays in the U.S. include bank accounts with $o opening requirements and no monthly service fees and competitive CD rates. The cons of banking with Barclays include no physical locations, no checking accounts, and limited services and products beyond banking.

Barclays Savings Account Review

Barclays online savings account.

Earn 4.35% APY with a $0 minimum opening deposit. Member FDIC.

no monthly service fee

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. High APY

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. No minimum opening deposit

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. No monthly service fees

- con icon Two crossed lines that form an 'X'. Must transfer money to external bank to access it

- con icon Two crossed lines that form an 'X'. Low mobile app ratings in the Apple store

The Barclays Online Savings Account is a solid free savings account and is a worthwhile choice if you'd like to open an account with Barclays and a competitive interest rate. However, Barclays doesn't offer a checking account, so you'll have to transfer money to an external bank account to access your money.

- No checking account or debit card, so you must transfer funds to an external bank account to access your money

- Compounds interest daily to maximize earnings

- Interest compounded daily, deposited monthly

- FDIC insured

Barclays Tiered Savings

Earn up to 4.80% Annual Percentage Yield (APY) with minimum balance requirements

no monthly maintenance fee

up to 4.80%

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. No monthly maintenance fees

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. No minimum opening deposit required

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. High APY at the highest tiers

- Check mark icon A check mark. It indicates a confirmation of your intended interaction. Interest compounds daily

- con icon Two crossed lines that form an 'X'. Requires a lot of money to earn highest tier of interest

- Online-only bank for U.S. customers

- Customer service available over the phone from 8:00 am ET to 8:00 pm ET every day of the week

- Accounts with less than $10,000 will earn 1.00% APY, accounts with at least $10,000 but less than $50,000 will earn 4.00% APY, accounts with at least $50,000 but less than $250,000 will earn 4.50% APY, and accounts with over $250,000 will earn 4.80% APY

- Interest compounds daily and deposits monthly

- Member FDIC

The Barclays Online Savings Account is a good account for easy opening requirements — you can open it for $0, and there aren't monthly maintenance fees. It pays more than the average savings account, but some online banks have 5% interest savings accounts available.

Barclays also offers a tiered savings account with a higher interest rate. Barclays Tiered Savings also has a $0 minimum opening deposit and no monthly maintenance fee, but you have to keep a high account balance to get the best APY.

Barclays CD Review

The Barclays Online CD offers strong CDs with competitive interest rates, regardless of which term you choose. Unlike most banks, it doesn't require a minimum deposit, so you can start with any amount. The bank also charges relatively low early withdrawal penalties should you need funds before your CD matures.

Barclays Credit Cards Review

Barclays has co-branded credit cards with many businesses, including JetBlue, Gap, American Airlines, Hawaiian Airlines, and Emirates. None have been selected for our best credit cards , though.

Barclays Personal Loans Review

Barclays offers personal loans, but you need to get an invitation to apply. The bank's personal loans website doesn't mention how you can get an invitation code.

Barclays vs. Ally

Barclays and Ally pay similar interest rates on savings accounts, and Ally pays slightly higher CD rates for most terms 3 years or longer. Interest rates can fluctuate, though, so this may change in the future.

If you are looking for savings account with budgeting tools, you might like Ally's bucket system, which lets you save for multiple goals in one savings account, such as "Emergency Fund" or "Vacation."

Something to keep in mind is that Barclays only offers a high-yield savings account and CDs. If you're looking for a bank to open a checking or money market account, then you'll prefer Ally to Barclays (which has neither).

Ally Bank Review

Barclays vs. Marcus

Barclays and Marcus by Goldman Sachs savings accounts have a lot of similarities: good interest rates, no monthly services fees, and no minimum opening deposits. If you'd like to withdraw money from either account, you'll need to transfer it to an external bank account, since neither has a checking option. It could be a toss-up between the two banks because the savings accounts are pretty much the same.

While the two banks offer similar savings accounts, there are a few clear distinctions between Barclays and Marcus CDs.

For example, Barclays lets you open a CD with $0, while Marcus CDs require at least $500 upfront.

If you'd like to open a no-penalty CD, you'll probably favor Marcus. Barclays doesn't have no-penalty CDs. It should also be noted that Marcus has some of the best no-penalty CDs . The Marcus No-Penalty CD pays competitive interest rates for no-penalty CDs and has several term options.

Marcus by Goldman Sachs Review

Why You Should Trust Us: How We Reviewed Barclays

To review Barclay's savings accounts, we used our bank account methodology . To rate CDs, we used our certificate of deposit methodology . Each account receives a rating between 0 and 5.

We evaluate ethics, customer service, and mobile apps when rating every type of account. Other factors considered depend on the type of account we're reviewing. For example, we look at whether a money market account offers access to your funds with an ATM card, debit card, and/or paper checks. For CDs, we look at term variety and early withdrawal penalties.

- Bank accounts

- Savings and CD rate trends

- How banks operate

- Certificates of deposit

- Savings accounts

- Checking accounts

- Bank reviews

- Main content

- Barclays Live

Weekly Insights

26 Jul 2024

Not everyone gets a medal

- Amid an equity sell-off, US economic data may show soft spots but remain solid overall. Meanwhile, signals out of Europe and China are weaker.

- With a steady diet of easing already priced into rates starting in September, the FOMC has little upside to do anything more next week than hint that a September cut is on course.

- July's euro area and national business surveys sent worrying signals on economic momentum, with weakness in manufacturing seemingly extending into services.

- We think that next week, the Bank of England will start the easing cycle with a hawkish cut, delivered with a 5-4 vote split.

- In Japan, we still expect a rate hike next week as wage/inflation developments back the Bank of Japan’s virtuous cycle scenario and prominent politicians voice support.

- In China, we think the recent relief from CNY depreciation pressures offered a window for this week's policy rate cut.

- We continue to see evidence that a gradual broadening of the tech upcycle is providing a back-loaded lift to Southeast Asian economies – and North Asia is losing momentum.

Get the latest report

Authorised clients of Barclays Investment Bank can log in to read the latest Global Economics Weekly on Barclays Live:

- Global Economics Weekly: Not everyone gets a medal

- Learn more about our Research services

- Important content disclosures

More from Barclays Research

Our Insights

View highlights of research from Barclays Investment Bank’s macroeconomic market experts and analysts, and other insights from across our businesses.

Powering Possible

See possibilities where others see challenges with a global bank that can help you harness the power of change to drive sustainable growth.

* We acknowledge and agree for Barclays to collect, use and otherwise process our/the Relevant Individual's Information in accordance with the Notice, other effective privacy terms and information processing terms agreed by ourselves/the Relevant Individual with Barclays, for the purposes set out therein, respectively.

* We acknowledge and agree that Barclays may disclose to any third party described in the Notice as a potential recipient of data outside mainland China our.the Relevant Individual's Information in accordance with the Notice, other effective privacy terms and personal information processing terms agreed by ourselves/the Relevant Individual with Barclays, and for the purposes set out therein, respectively.

I consent to my email address being used by Barclays to provide me with personalized advertisements on third-party websites and social media platforms, as described in our Privacy Notice.

An email was sent to you at the address provided. Complete your subscription by clicking the link provided to verify your email address.

Sorry there was a problem. Unfortunately your subscription to our newsletter has encountered an error.

In addition to the cookies we use on our website, we also use cookies and similar technologies in some emails and push notifications. These help us to understand whether you have opened the email and how you have interacted with it. If you have enabled images, cookies may be set on your computer or mobile device. Cookies will also be set if you click on any link within the email.

In addition to the cookies we use on our website, we also use cookies and similar technologies in some emails and push notifications. These help us to understand whether you have opened the email and how you have interacted with it. If you have enabled images, cookies may be set on your computer or mobile device. Cookies will also be set if you click on any link within the email.

Please review and manage your email cookie settings below. For more information, please read our Cookie Policy . Please select 'Save and Subscribe' below to remember your email cookie preferences and subscribe to the newsletter.

Barclays Renews Long-Standing Partnership with Hawaiian Airlines

News provided by

Jul 26, 2024, 07:00 ET

Share this article

Partners since 2013, Hawaiian Airlines ® and Barclays US Consumer Bank will continue their consumer and small business credit card programs in a multi-year agreement.

WILMINGTON, Del. , July 26, 2024 /PRNewswire/ -- Barclays US Consumer Bank, a leading credit card issuer and financial services partner, announced today the renewal of its decade-long co-branded credit card program with Hawai'i's largest and longest-serving airline, Hawaiian Airlines.

Under the newly signed agreement, Barclays will continue to issue the Hawaiian Airlines World Elite Mastercard® for consumers; and the Hawaiian Airlines World Elite Business Mastercard®, for small businesses.

"The contract extension with Hawaiian Airlines builds upon the strong history and collaborative nature of our partnership dating back to 2013 and will ensure the program is well positioned for continued growth," said Denny Nealon , CEO, Barclays US Consumer Bank. "Barclays has a proven track record of winning and growing partnerships—and our long-standing relationship with this incredible airline supports Barclays' ambition to be a partner of choice for America's best brands."

"Our extended partnership with Barclays ensures our cardholders will continue to enjoy exceptional benefits and superior value when earning HawaiianMiles and traveling to, from or within Hawai'i," said Avi Mannis , Executive Vice President and Chief Marketing Officer at Hawaiian Airlines.

The Hawaiian Airlines World Elite Mastercard is one of the fastest ways to earn HawaiianMiles that never expire. Primary cardmembers receive two free checked bags on eligible flights, a $100 annual companion discount and benefit from Hawaiian's 3/2/1 earn rate (3x on Hawaiian Airlines Purchases, 2x on Gas/Dining/Grocery, and 1x on all other). Hawaiian Airlines is currently awarding new cardmembers 70,000 bonus HawaiianMiles after qualifying purchases.

Hawaiian Airlines has also partnered with a variety of companies to give cardmembers even more ways to earn miles every day through their Buy and Fly program. HawaiianMiles Buy and Fly is a collection of local and national shops and restaurants that offer bonus HawaiianMiles for purchases made with the Hawaiian Airlines World Elite Mastercard. Each Hawaiian Airlines card comes with contactless technology featuring a core made with recovered ocean-bound plastic, building on the airline's commitment to environmental stewardship.

About Barclays US Consumer Bank Barclays US Consumer Bank is a leading co-branded credit card issuer and financial services partner in the United States that creates highly customized programs to drive customer loyalty and engagement for some of the country's most successful travel, entertainment, retail, and affinity institutions. The bank offers co-branded, small business and private label credit cards, installment loans, online savings accounts, and CDs. For more information, please visit www.BarclaysUS.com .

About Hawaiian Airlines

Now in its 95th year of continuous service, Hawaiian is Hawaiʻi's largest and longest-serving airline. Hawaiian offers approximately 150 daily flights within the Hawaiian Islands, and nonstop flights between Hawaiʻi and 16 U.S. gateway cities – more than any other airline – as well as service connecting Honolulu and American Samoa , Australia , Cook Islands , Japan , New Zealand , South Korea and Tahiti.

Consumer surveys by Condé Nast Traveler and TripAdvisor have placed Hawaiian Airlines among the top of all domestic airlines serving Hawaiʻi. The carrier was named Hawaiʻi's best employer by Forbes in 2022 and has topped Travel + Leisure's World's Best list as the No. 1 U.S. airline for the past two years. Hawaiian has also led all U.S. carriers in on-time performance for 18 consecutive years (2004-2021) as reported by the U.S. Department of Transportation.

The airline is committed to connecting people with aloha by offering complimentary meals for all guests on transpacific routes and the convenience of no change fees on Main Cabin and Premium Cabin seats. HawaiianMiles members also enjoy flexibility with miles that never expire. As Hawai'i's hometown airline, Hawaiian encourages guests to Travel Pono and experience the islands safely and respectfully.

Hawaiian Airlines, Inc. is a subsidiary of Hawaiian Holdings, Inc. (NASDAQ: HA ). Additional information is available at HawaiianAirlines.com . Follow Hawaiian's Twitter updates ( @HawaiianAir ), become a fan on Facebook ( Hawaiian Airlines ), and follow us on Instagram ( hawaiianairlines ). For career postings and updates, follow Hawaiian's LinkedIn page.

For media inquiries, please visit Hawaiian Airlines' online newsroom .

SOURCE Barclays US

Modal title

Also from this source.

Barclays Releases 2024 Travel Rewards and Loyalty Report

Personal travel is top of mind for many consumers this year and rewards programs will make all the difference, according to a survey of 1,000 US...

Barclays Awards $255,000 to Small Businesses in Its Fourth Annual 'Small Business Big Wins' Promotion

Barclays US Consumer Bank today announced Diversability LLC as the winner of its fourth annual "Small Business Big Wins" promotion and the recipient...